This essay was written by Matt Dion. In addition to being a content consultant at Naavik, Matt is a product manager at EA Mobile.

Source: Crunchbase

Last month, Turkish casual games developer Dream Games raised $155M in a Series B round, valuing the company at $1B. This made Dream Games the industry’s latest “unicorn” — an impressive feat for an early-stage games developer with just one title to its name (the massively successful Royal Match). However, what really caught the attention of industry watchers was the speed at which it happened: Dream Games had previously raised its $50M Series A just 3.5 months earlier.

Even more interesting is the fact that Dream Games is just the latest in a string of games industry startups to attract the attention of venture capitalists. In the last year and a half, VC interest in the sector has reached a fever pitch.

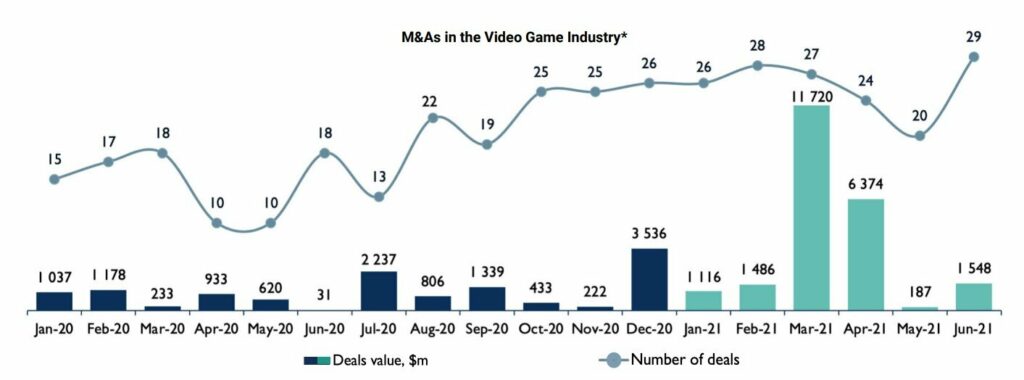

In their recent Gaming Deals Activity Report H1 2021, our friends at InvestGame counted 263 closed private investments in the first half of 2021 alone, compared to 161 in H1’20. More than 64% of those private placements came at an early stage, representing roughly $1.1B in total value.

What is it about the games industry that has proven attractive to venture capital firms? Why are we seeing more deals at ever-greater valuations, and why now?

The Present State of Gaming VC

Before diving deeper, let’s first orient ourselves within the broader games dealmaking landscape. According to InvestGame, private investments (of which venture capital is just a fraction) made up 56% of all closed deals in H1 ‘21 by volume. However, this represents just 10% of the $44.2B in total value in the same time period.

Venture capital firms have been making a large number of small bets across the industry, hoping that a few of them might provide a significant return for their funds. Looking at the top VCs by deal volume in the first half of 2021, we see that the ten most active firms closed 63 deals, accounting for nearly a quarter of all private investments during the period.

These recent increases in venture capital activity in gaming can be attributed to a confluence of trends underpinning the industry. I’ve roughly bucketed these trends into two areas, which I’ll unpack below:

- Macro Trends

- Likelihood of an Exit

Macro Trends

Why do venture capitalists even care about gaming in the first place? For one, gaming has become increasingly ubiquitous. There are nearly three billion gamers worldwide, representing more than a third of the entire global population. That number is expected to continue to grow over the coming years, and with that massive player base has come greater societal acceptance, particularly as so many people have been stuck at home during the COVID-19 pandemic. Furthermore, gaming has proven itself to be a growth industry. Gaming revenues are already larger than the film and music industries combined, and expected to continue growing.

VCs invest on long time horizons. Most venture funds have a period of 10 years or more during which they invest their capital and return profits to their investors. While the time required to develop AAA games is certainly increasing, it does not necessarily match the timelines of these VCs — many of whom may be wary of getting involved in what’s traditionally been viewed as a hits-driven business. However, gaming businesses are increasingly sprouting up on the bleeding edge of technology, where the macro trends that do fit VC timelines are better represented. Trends often referenced on VC Twitter such as blockchain technology, cryptocurrency, the Creator Economy, user-generated content, and the Metaverse all have roots in gaming. That, in turn, has captured the attention of VCs in search of the next big thing.

As our analog and digital lives merge ever closer, games are often the first avenue for experimenting with new forms of disruptive technology. One of the great insights from the work of Clayton Christensen (Harvard professor and author of The Innovator’s Dilemma) is that disruptive innovations are often dismissed as toys in their early stages, improving at faster rates than users’ needs might dictate.

Viewing recent trends through this lens, many recent VC investments in the gaming space begin to make sense. Blockchain technologies, for example, underpin many notable investments in the games space: from the infrastructure play of Forte, to the Play-to-Earn model of Axie Infinity and Yield Guild Games, to the NFT & collectibles market of Dapper Labs’ NBA Top Shot.

We can draw similar parallels to the continued improvements in game engine and device technologies (photogrammetry, volumetric video, spatial audio, raytracing, haptics, mixed reality, etc.) and the proliferation of venture-backed Metaverse startups (Manticore Games, Rec Room, and Playable Worlds, to name just a few).

Macro trends following the emergence of these and other disruptive technologies will continue to drive venture capital firms to invest in gaming startups. This is especially true for generalist funds that may not be solely dedicated to the space, as they are more likely to be familiar with the investment theses around these technologies than the peculiarities of games investing. Even still, gaming companies represent the vast majority of deals in the space. According to InvestGame, nearly 75% of deal value (VC or otherwise) in H1 ‘21 went to gaming companies, as opposed to platform and tech, esports, or other gaming-adjacent businesses.

This is just a part of the explanation for our current games venture capital bonanza. Another important development is occurring at the opposite end of the startup journey: the exit event.

Likelihood of an Exit

While investing in macro trends is all well and good, venture funds must ultimately provide returns to their investors. Here, too, gaming startups have provided VCs with plenty of reasons to be excited. The games industry has been awash in exits lately, driven by increasing levels of consolidation and a receptive public market. Furthermore, the magnitude of recent successful exits — such as those of Roblox and Unity — proves that gaming is operating at a larger scale than ever before. Between higher likelihoods of exits and higher magnitudes of upside potential, it’s easy to see why the gaming venture ecosystem continues to flourish.

The recent wave of industry consolidation can be decomposed into multiple strategies across several gaming verticals. Companies are being snapped up for a wide variety of reasons, each of which deserve their own analyses (and some of which I’ve linked below):

- PC/Console publishers are beefing up their mobile offerings (EA, Take Two)

- Some platform holders are locking in exclusives to attract and retain players (Microsoft, Epic), while others are seeking to expand their technical capabilities (Unity, Roblox)

- Mobile publishers are shifting to adtech (Zynga)…

- ...and adtech companies are shifting to mobile development (AppLovin)

- Holding companies are buying all manner of game developers across platforms (Stillfront Group, Enad Global 7, Modern Times Group, Embracer Group)

- Tencent is investing everywhere across the industry as it fends off challenges on multiple fronts within its home country and expands internationally:

This is just a sampling of the companies vying to acquire game developers and games tech firms. With so many M&A partners seeking to execute a variety of acquisition strategies, the potential for an exit event is high for a venture-backed firm with a strong team.

Furthermore, public markets have become more favorable to the games industry, pushed to new highs by COVID-related tailwinds and the increased acceptance of special purpose acquisition companies (SPACs). This provides another viable exit strategy for venture-backed games companies that would have been far less likely just a few years ago.

Recent public offerings in the games industry have spanned multiple verticals:

While not all of these have been massively successful public debuts, the sheer volume of gaming IPOs, SPACs, and direct listings compared to previous years is indicative of the appetite on Wall Street for exposure to the sector. This increasing track record gives VCs additional data to support future investments in the games industry. Clearly, the environment for venture-backed games industry investments is extremely favorable. However, as outlined above, this statement paints broad strokes over a number of underlying trends and investment strategies.

While we can safely assume that venture capitalists will continue to take big swings at macro trends with huge upside potential, investment in high-growth studios like Dream Games has historically been much less consistent. How are VCs thinking about investments in game studios, specifically, and what can we learn about their approach to content-driven investments from recent history?

Investments in Game Studios

Gaming studios have been pushing back on the sentiment expressed in the Tweet above for years now. Many investors are quick to lump games in with other forms of media that are also often overlooked by venture capital dollars. Yet gaming is a content-driven industry; just one successful game release can drive immense value for a company and therefore cannot be ignored outright by venture capital. One needs to look no further than companies like Riot Games, Krafton, or Sea Limited to see how a single title (League of Legends, PUBG, and Free Fire respectively) can be the catalyst for an incredible growth business.

There have been many different approaches to investing in games studios in recent years, as venture capitalists sought to back companies with differing competitive advantages. Often, a quick look at a studio’s cap table will provide insight into these varying strategies. In the case of the aforementioned Dream Games, for example, we can see several approaches at play in the co-leaders of the latest round: Index Ventures and Makers Fund.

First, let’s take a look at Index Ventures. As they state on their website, “[o]ther firms invest in deals, Index invests in people.” Betting on strong founding teams is an approach taken by many VCs in gaming, and for good reason -- founding teams that come from studios and publishers with proven track records are much more likely to succeed than those who do not, as they often possess significant institutional knowledge. Dream Games is no exception here, boasting a founding team made up of veterans from casual games powerhouse Peak Games, creators of highly-successful match games like Toy Blast and Toon Blast.

Skills related to building and operating game teams, communicating with and fostering fan ecosystems, and designing and marketing games IPs help not only to de-risk investments for VCs, but also to attract early interest from fans of the creators themselves. A great example of this is the hype surrounding venture-backed startups like Playable Worlds (led by Raph Koster, designer of titles like Ultima Online and Star Wars: Galaxies) and Frost Giant Studios (helmed by Starcraft and Warcraft veterans Tim Morten and Tim Campbell), to name just two.

Beyond backing strong founders, Index Ventures also aims to invest globally. This is again evident in Dream Games (based in Turkey) as well as in other impressive games studios they’ve backed in the past:

- King (Sweden)

- Supercell (Finland)

- Bigger Games (Turkey)

- Supersolid (UK)

Makers Fund has also adopted a global approach, with a variety of interactive entertainment investments across Europe and Asia.

Having a global scope makes a lot of sense when investing in game development. For one, the global population of gamers is growing ever-larger, and there are business opportunities in serving those players with hyper-local games and live ops (more on this later). Furthermore, the costs of game development can be quite high, so finding venture-backable businesses in emerging markets can help to de-risk investments. A great example of this is the BITKRAFT Ventures-backed LILA Games, a studio which has chosen to base most of its operations in India while its founders work remotely from the United States. For a group developing a mobile shooter (a genre typically associated with high development costs), this global approach could prove to be a major selling point for VCs (in addition to the company’s highly-experienced founding team).

Another differentiator driving VC investment in games studios is business model innovation. This has been a factor in games funding at least since the advent of free-to-play games, with companies like Riot Games and Zynga raising venture capital rounds more than a decade ago. As readers of Master the Meta well know, the shift to free-to-play business models kicked off a tectonic shift in the gaming landscape, resulting in massive returns for successful early adopters and their venture capital backers.

Fast forward to today, VCs are still on the lookout for new business models that might drive similar growth. Blockchain gaming is one area that has attracted significant interest in that regard, with the trading economy framework of Mythical Games and the scholarship approach of Yield Guild Games making major waves (to name just a few in a recent surge of blockchain gaming investments). Mythical Games’ Blankos Block Party, which recently debuted a $300 NFT collaboration with British fashion house Burberry, sold out its collection in 30 seconds. Yield Guild Games, meanwhile, has driven interest in the NFTs of Axie Infinity sky-high, allowing its scholarship recipients to earn a living playing the game. While Yield Guild Games isn’t a game developer, per se, it’s easy to see how an innovative business model such as this could be incorporated into a game’s development process. Furthermore, the developer behind Axie Infinity, Sky Mavis, has itself been a recent recipient of venture.

While innovating on business models can have massive upside, it’s also potentially risky. In some cases, startup game studios are better off applying proven business models in interesting and new ways, seeking out new or underutilized platforms as a launchpad for their titles. Creating the “killer app” for a platform can give studios important first-mover advantages over other new entrants, while also growing the size of the total addressable market by bringing new players to the platform. Rec Room (VR), Gamefam (Roblox), Mainframe (Cloud Gaming) and Tilt Five (AR Tabletop) are all examples of recent venture-backed startups utilizing this approach.

Finally, it’s worth noting that VCs are willing to bet big on a mix of several of the strategies outlined above. In fact, this may be the most common approach, as being able to check multiple boxes off this list will ultimately give investors more confidence in making a multi-billion dollar investment. One such example of this is the $100 million investment by Makers Fund, Sequoia Capital, and others in Playco — a startup seeking to operate on multiple non-traditional games platforms (✔) while taking advantage of technological improvements and improved margins on the instant games business model (✔). The company also boasts an impressive pedigree (✔), counting a Zynga co-founder, DeNA director, and HTML5 gaming pioneer among its ranks. And just to check that final box, they’re also global, operating fully remotely from Seoul, Tokyo, Los Angeles, and San Francisco. Given what we’ve outlined above, it’s no wonder the company was able to put together such an impressive cap table and pull in a $1 billion valuation.

We’ve now walked through several different strategies taken by venture capital firms when investing in games studios, and we’ve already established that the current market is extremely favorable to VC investment in games startups. Should we expect this breakneck pace of funding to continue?

The Future State of Gaming VC

When considering what the future may hold for venture capital in the games industry, we should consider not only the current trends in games funding but also the direction of venture capital as a whole.

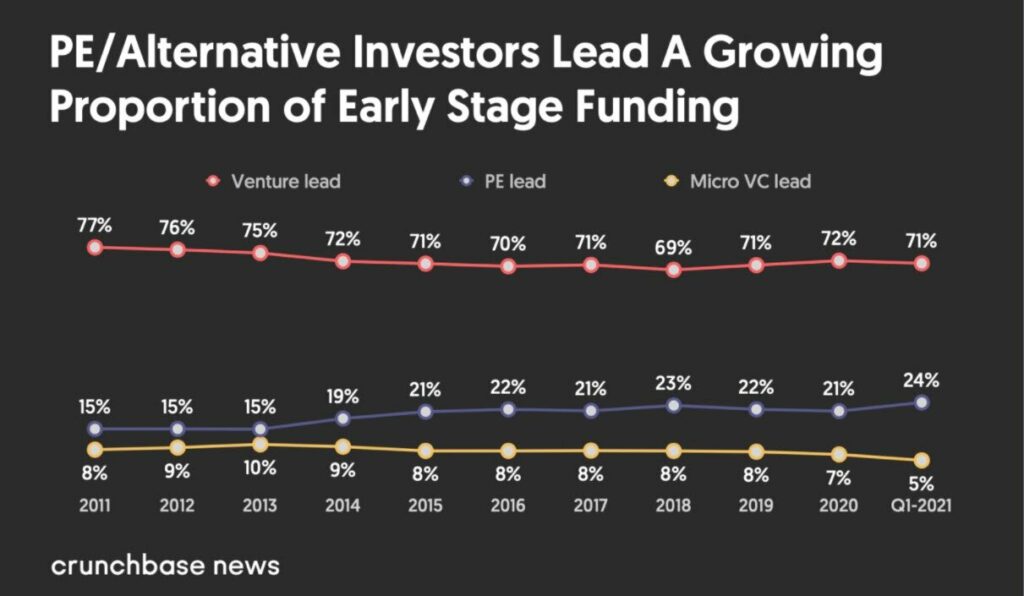

While gaming has had an incredibly strong year thus far, the broader VC ecosystem has also experienced record-breaking growth. However, there are some who believe that this may not be sustainable. Recently, Sam Lessin of Slow Ventures predicted “The End of Venture Capital as We Know It”, hypothesizing that 2022 will see nontraditional tech investors invest more in private tech companies than traditional VCs. To that end, there have certainly been warning signs at the early stages, as private equity investors have gained ground on venture capitalists with regards to deal leadership:

VCs are also being squeezed from the other direction, as the recent phenomenon of so-called “solo capitalists” has increased the level of competition to get onto coveted cap tables.

The implication of all this is that venture capital firms may need to find new ponds to swim in. While Lessin’s piece is more focused on SaaS and software, one could argue that gaming businesses are not so distant relatives. Games businesses may not attract the same level of private equity or other institutional investment that SaaS companies do, but we have already seen the rapid consolidation among gaming titans like Tencent, EA, Microsoft, and others. These large entities will continue to encroach on the early-stage playing field, and to that end, I expect gaming VCs to find more specialized areas to operate in, where they can potentially offer greater value-add to entrepreneurs.

One area where we have already seen a migration of funding is in region-specific backing. VCs like Lumikai (focused on the Indian games industry) and The Games Fund (Eastern Europe) are leading the way in this regard. Game publishers are also getting involved, with companies like Carry1st (Africa) and PLAY Interactive (Southeast Asia) raising money and opening their own coffers to catalyze game development in their respective focus regions. As the games industry continues to expand to all corners of the globe, I would not be surprised to see additional dedicated games funds begin to focus on similarly underserved markets.

We should also expect to see gaming venture capital differentiate beyond simply geographic focus. There are already a number of sector-agnostic funds dedicated to specific demographics, such as those investing in women-led ventures, BIPOC founders, LGBTQ+ entrepreneurs, and more. It’s not crazy to think that in the future we may see funds of a similar vein sprouting up to support gaming companies seeking to serve these demographics. Indeed, the gaming industry could benefit from a healthy dose of diversity.

I suspect that we may see more funds dedicated to tech-driven gaming investment theses, too, such as blockchain gaming or metaverse funds. In fact, we are already seeing traction in both of those areas, with BITKRAFT Ventures and Delphi Digital teaming up on crypto gaming, and Roundhill Investments partnering with Makers Fund’s Matthew Ball and others on its Metaverse ETF.

While the funding mix will likely continue to evolve, venture capitalists will have no shortage of investment opportunities available to them. In fact, there are more gaming entrepreneurs today than ever. Talented games industry leaders with proven track records are increasingly choosing to pursue entrepreneurship over the safety of a job with an industry incumbent. Several factors are contributing to this trend. First and foremost is the friendly environment for gaming investments, outlined above. Not only is it easier to get funded and make a living with a games studio, but the work itself has been simplified: remote work has allowed talent to collaborate from anywhere, while a variety of services have popped up to support smaller developers, assisting with everything from analytics to market research to user acquisition funding.

Contrast that with the work environments at the incumbent publishers, platforms, and developers. Some continue to urge a return to in-office work. Others have enabled toxic, sexist, and unsafe workplaces to exist. And others overwork their employees with long stretches of “crunch”. Is it any wonder that talented game developers are choosing to go the startup route?

Given this abundance of entrepreneurial talent, I suspect that the gaming industry will continue its hot streak of investments. However, I would not be surprised to see a leveling off in the participation of venture capitalists specifically, given the market pressures outlined above. Entrepreneurs have more avenues than ever before to raise funding for their games businesses, including one method we have not even covered here: leveraging the Creator Economy. Developers behind hits like NoPixel and Beat Saber are perfect examples of this.

Will Dream Games be the last games company to raise a mega round from venture capital firms? Certainly not. But I suspect that we may be nearing a peak (or perhaps even a plateau) for VC participation, as a host of other investors seek to cash in on the red-hot gaming market.