Source: Coinmarketcap.com

Download the Full PDF Report

Sign up with your email address to receive the full PDF report, and sign up for Naavik Digest.Sign Up

Outline

- The Road to Mass Adoption: A quick review on where blockchain gaming is on the road to mass adoption + commentary on blockchain gaming’s key macro metrics (UAWs, NFT transaction volumes, and number of blockchain games ).

- The Fall of P2E Gaming and Market Speculation: Analyzing the current state of the P2E market after Axie Infinity’s fall and land assets’ devaluation too, and highlighting how projects are building today.

- A Radically Different Funding Environment: Analyzing key funding trends for the space, and how the pace of deal activity has not only slowed down, but also both teams and VCs are getting smarter + our take on the future of guilds.

- New Frontiers and the Path Forward: Going over the most significant trends that are forging the space’s future, such as wallet infrastructure, game distribution mechanisms, industry-wide talent migration, the evolution of product thinking from P2E to F2O, other key product trends and regulation.

Executive Summary

Even though blockchain gaming continues its struggle out of the broader crypto bear market, Q3 2022 was a quarter filled with much game building, market movement, funding corrections, and learnings. This report looks at how blockchain gaming fared over Q3 2022, key trends that emerged, and where the future of the space is headed.

Here is the executive summary:

- The market has generally been stagnant from a pricing perspective, and the old guard of games is waning. At the same time, there were sprinkles of small wins and a lot of steady anticipation for the future of the space.

- Blockchain gaming still has a long way to go for mass adoption. This is seen in stagnating Unique Active Wallets (UAWs, ~1M), NFT transaction volumes (~$500M), and the number of blockchain games (~2,000).

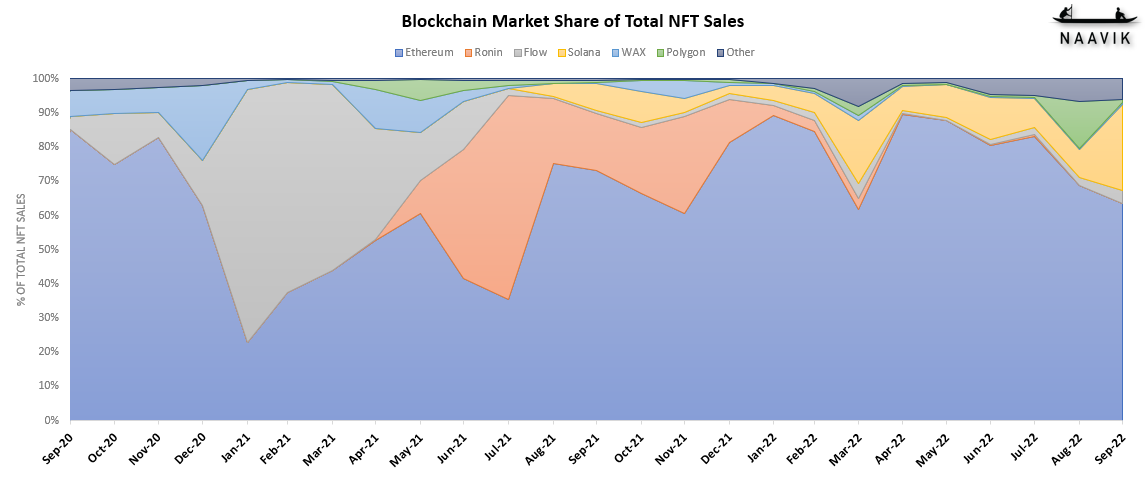

- In terms of blockchain market share (based on secondary market NFT sales), Ethereum still holds the vast majority (~60%). But that is not stopping L1s and L2s (Solana, Polygon, Immutable – some of which are built on top of Ethereum) from actively competing and striving to be the #1 choice for blockchain game developers to build on.

- There’s a strong bifurcation in blockchain gaming right now. Play-to-earn (P2E) gaming has fallen with all once-major projects losing upwards of 90% of their market capitalization over the course of 2022. There is also a similar downtrend across other speculative game-related assets – most notably virtual land NFTs belonging to games that are yet to launch. However, the next era of fun games that are far less focused on earning are steadily being built by many talented teams around the world.

- Blockchain gaming is moving towards its third era of games:

- The first era of blockchain gaming primitives was defined by CryptoKitties, which showcased what NFTs and “player” ownership could mean, but it was fundamentally held back by the Ethereum network’s complete lack of scalability.

- The second era was defined by Axie Infinity, which built a real game and used scalability solutions, but its fatal flaw was economic design — incentivizing unsustainable earning over fun.

- The third era of crypto games will build off of the previous two eras — using various scalability solutions and sidestepping the largest economic flaws while prioritizing fun.

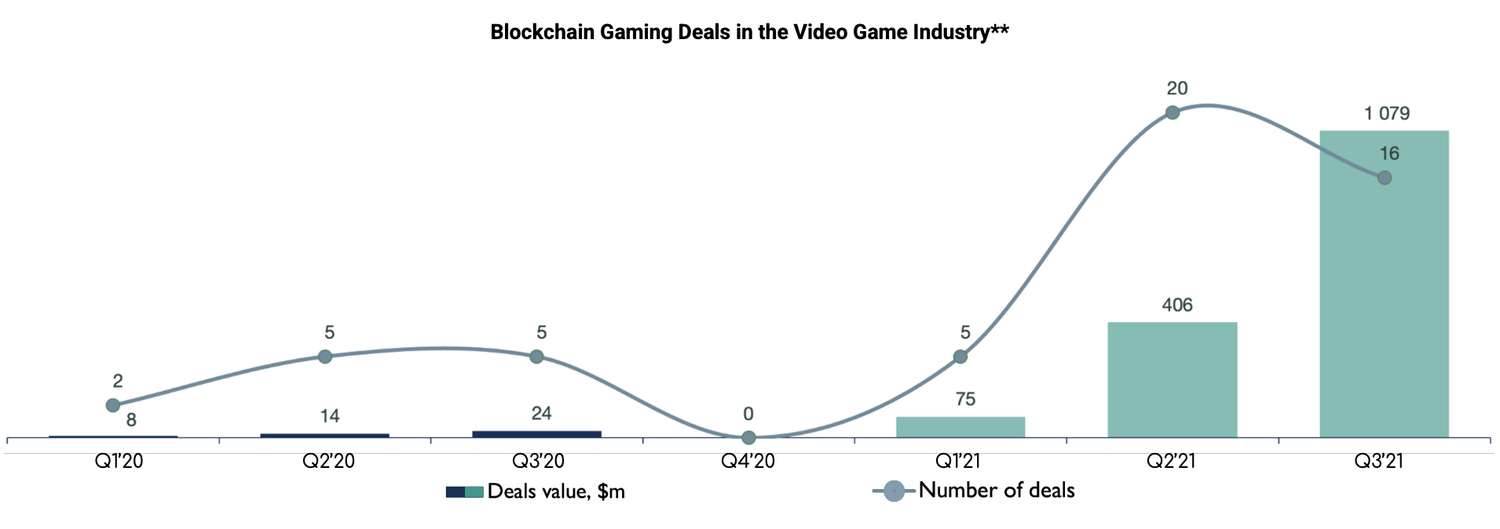

- Q3 2022’s funding environment looks radically different. This is the first quarter in which blockchain gaming has seen negative YoY growth metrics. While the Q3 2022 total deal number was up 2.6x YoY (58 vs. 22), the total deal value was down -19% YoY ($875M vs. $1.1B). The QoQ growth metrics were also down, indicating the continuation of the 2022 market correction that we began to see at the start of 2022.

- The buzzword for almost every guild currently is ‘pivot’. To prevent most guilds from going under, we believe that guilds will need to adapt from their first generation business model (seeking yield from renting out in-game assets) to focus on one or more of 5 key areas to move towards Guild 2.0 – Community, Investment Management, Technology Products, Value-Add Services and Content.

- Overall, it seems like the blockchain gaming deal market continues to mature into its next stage, wherein the companies garnering most of the funding attention are no longer the ones building infrastructure, but rather the blockchain gaming studios that can produce engaging content that makes use of blockchain gaming infrastructure.

- Of all the infrastructure solutions out there, the one that will truly unlock mass adoption of blockchain gaming (besides the blockchains themselves and perhaps marketplaces) will be one that is closest to the players and likely the most cared about: wallets. Sequence by Horizon and Stardust Vault by Stardust will be two to keep an eye on.

- Major platforms are slowly warming up to the idea of distributing blockchain games, or at least finding ways to take a cut. Epic Games Store hosting Blankos Block Party and Apple allowing the sale of NFTs (albeit in a limited fashion) is the start of a movement that will increase the presence of NFTs and web3 with more consumers. Enabling the mass distribution of blockchain games is very much an important catalyst for mass adoption.

- The migration of traditional game developer talent to build the blockchain games of tomorrow has begun. While this migration will be slow and steady (and may upset certain traditional gamers), the curiosity about blockchain gaming and the need to skill up for a potential future of gaming are both high. The impact of this talent migration should result in games that are not only more fun to play, but also are built on the back of traditional gaming best practices (accelerating the quest for economic sustainability).

- Best practices that define the future of blockchain gaming are very much in the making with Free-to-Own (F2O) being the fourth evolution after Play-to-Earn (P2E), Play-and-Earn (P&E), and Play-and-Own (P&O).

- The killer feature of F2O is the simple fact that it dramatically lowers barriers to entry by offering NFTs for free and not gating game access with sometimes absorbently high NFT (of multiple NFTs) purchase prices. This could be an important catalyst for accelerating mass market adoption.

- Other important product trends include on-chain gaming, F2P blockchain gaming, evolving tokenomics models, genre and audience expansion across web3 games, the Asian blockchain gaming scene, user-generated content (UGC) and artificial intelligence (AI) in blockchain games.

- While 2020 and 2021 were truly the wild west years in terms of what developers and players could get away with, these years were also fraught by major value destruction hacks and scandals that cannot be turned a blind eye to. Regulation was always coming, but regulatory bodies have clearly started to take notice in 2022, with the SEC’s investigation into Yuga Labs becoming a figurehead.

#1: The Road to Mass Adoption

To understand where we are today on the road to mass adoption of blockchain gaming, let’s start by looking at how Q3 2022 fared. At a very high level, there has been significant funding, building, and learning from prior mistakes. And while the broader space has been in a slump – and many traditional gamers remain skeptical – there is currently a waiting game for the next wave of new releases to take the market to the next level.

The months from July through September were pretty similar in their behavior. In short, the market has generally been stagnant from a pricing perspective, and the old guard of blockchain games is waning. At the same time, there were sprinkles of small wins and steady anticipation for the future of the space.

Some key macro highlights from Q3 2022 include:

- Macroeconomic conditions, reduced interest in NFTs, and a lack of high-quality published games kept the market from roaring back, but portions of the ecosystem showed ongoing development that was worth celebrating. There is also a strong sense of pent-up anticipation for the next big wave, but it comes in the face of a weak crypto market, not to mention global macroeconomic risks.

- While none of the months experienced any industry-changing game releases or NFT hype, positive seeds were starting to germinate. Behind the scenes, many teams quietly worked hard to build new web3 games and so-called metaverse projects. It’ll take time to see the fruits of that labor — in many cases, a couple of years — but even as soon as the next few months, we’ll see more new games hit the market.

- Both Bitcoin and Ethereum showed signs of recovery, “the merge” — Ethereum’s switch from proof-of-work to proof-of-stake while making the network more deflationary — is now complete, and even contagion from the previous Luna crash is comfortably in the rear-view mirror. That said, the rising demand for blockspace far outstrips what Ethereum can cheaply supply, and chains like Immutable, Polygon, and Flow are starting to make increased strides forward.

- Casual and hypercasual games have slowly taken over the blockchain gaming charts. This trend will likely continue until more notable games come out with a bang, as Axie Infinity did.

- Fundraising generally dipped as it was down both quarter-over-quarter and year-over-year, which showcased a continued market correction trend amongst eager investors. At the same time, funding is still relatively strong on a broader scale, and there’s lots of dry powder. Those left are nearly all in it for the long-term (not speculators) despite the risks (such as regulatory uncertainty).

Going a layer deeper, let’s try to quantify where the blockchain gaming space stands today by looking at three key mass adoption metrics: Unique Active Wallets (UAWs), NFT Transaction Volumes, and the Number of Blockchain Games.

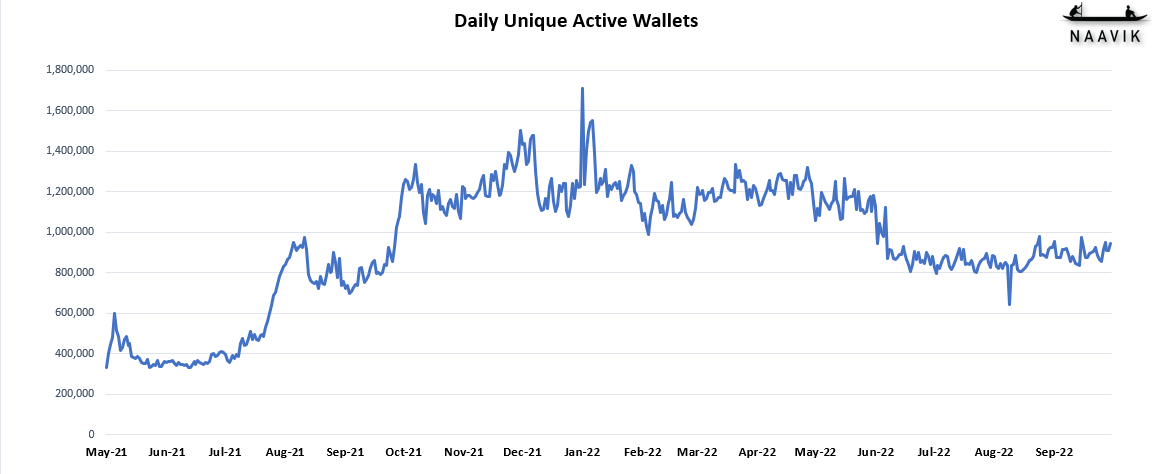

Unique Active Wallets

All in all, the short-term trend for UAWs shows stagnation, while long-term, it still trends upwards, albeit slowly and non-linearly. Given that UAWs are close to 1M, mass adoption from this metric’s perspective is still some time away.

More specifically:

- Per DappRadar, blockchain gaming daily unique active wallets (UAWs) has been mostly flat the entire summer, but it’s clearly down quarter-over-quarter (Q3 vs Q2 2022), and it could continue as such throughout the fall. However, given the number of games hitting alpha and beta status, we may see an uptake during 2023.

- While most of the more traditional P2E games have fallen, casual games (like Solitaire Blitz and Trickshot Blitz) and hypercasual games and platforms (like Gameta) have managed to find enough of a user base to make up for the declines elsewhere. Of course, it’s tough to tell if these “casual” players are new blockchain players/wallets — or if existing players are biding their time until more exciting releases occur or are simply bots. Given the number of high-quality casual mobile games that already exist, we assume that most adopters are still in it more for the money than fun. This will need to change if UAWs are to multiply from here.

All that said, UAWs are not a perfect indicator of active users. A user can have more than one wallet — potentially overestimating actual user activity. Conversely, a user can play a game but not transact with a blockchain over some time. Bots are also common across many games due to their earning ability and often appear in UAW numbers. Decentraland well articulated these issues and caveats with the metric in their recent blog post, where DappRadar underestimated Decentraland’s daily active user base by a 250x factor. Of course, this 250x ratio can’t be extrapolated to all games, given the radical differences in how games compel players to interact with blockchains. Despite UAWs being a flawed metric, its trends are noteworthy and can’t be ignored.

Whatever the perfect metric is, it is safe to say that blockchain gaming’s audience is still relatively tiny and has a long road ahead to mass adoption.

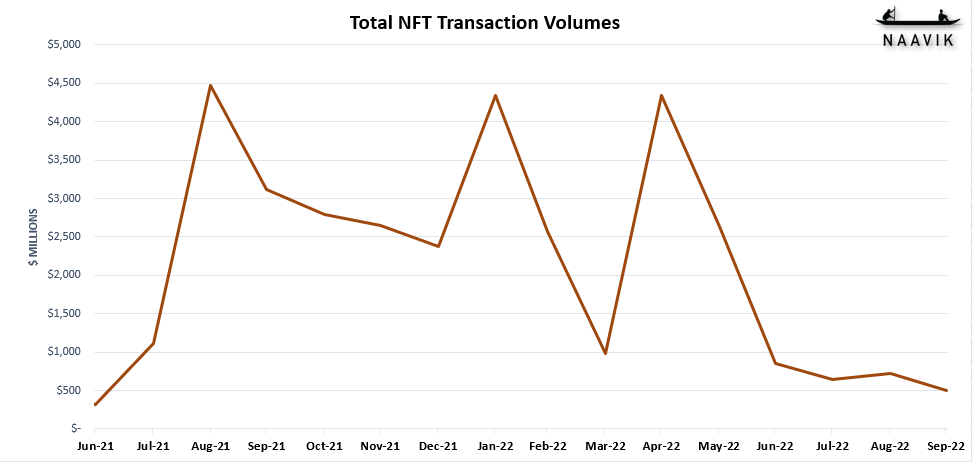

NFT Transaction Volumes

In general, it’s true that most (but not all!) of the speculation has dwindled by now — and hopefully, that means we’re nearing a bottom — but we’re also seeing tremendous improvements across infrastructure, tooling, and platforms that are laying the foundation for the next wave of more justifiable growth.

More specifically:

- As usual, monthly transaction volumes often depend on one or two large projects driving up the entire market, which didn’t happen over Q3 2022. According to Cryptoslam, total NFT transaction volumes on secondary markets (excluding primary sales) fell -30% over September, reversing the small gain experienced in August. Of course, these recent monthly changes look minor when compared to the massive swings experienced earlier this year and last year. We expect some future months with large volume spikes, but it will take some time for breakout hits to bring the masses back and for confidence in higher NFT valuations to return.

- Ethereum — which completed its “Merge” network upgrade — continues to show diminished dominance in total NFT sales as other networks and layers take more market share. Much of it naturally shifts over to Layer 2s on Ethereum (like Polygon and Immutable), which is good for the blockchain. Still, Solana, a competing Layer 1, also experienced some market share gains, especially over September 2022. As Ethereum has faced problems around high gas fees, Solana has continued to be a place for new NFT projects that don’t feel as attached to the Ethereum ecosystem. And while Solana has faced its share of network reliability issues, those may not have a strong impact on the simple minting and trading of NFTs as it does on games or dapps requiring frequent stable transactions.

- Polygon corrected back from the very outsized burst of activity over August 2022, partly due to OpenSea’s Seaport integration with Polygon and a single 65x transaction day for the Uniswap listing on Cryptoslam. It remains a network with huge potential given the technical progress, major business development wins (Starbucks, Meta, Adobe, Stripe, and more), number of games, and other NFT projects.

- Even though Ronin saw a minor bump from Axie Land activity in July 2022, it saw a massive drop from $5.04M to $0.94M over August 2022 as Axie Infinity Classic wound down and Origin Season 0 required recreation of all marketplace listings. It finally dipped to a meager $0.17M in volume over the quarter due to its entire existence depending on the success of Axie Infinity. Sky Mavis certainly has the money to try and turn things around, but despite the attempts at funding other Axie ecosystem projects, it has yet to prove why Ronin has a solid future. Read Part 1 and Part 2 of our Axie Infinity deconstructions to learn more.

- Immutable has been displaying notable growth due to increased activity around token staking and Gods Unchained. Its volume went from $5.2M in July 2022 to $28.7M in August 2022, and we expect it to continue growing. While the chain is still primarily home to Gods Unchained, the release of the GameStop NFT marketplace and respective wallet (which leverage the L2) has also helped boost interest. Eventual game launches, such as Illuvium and Guild of Guardians, should also significantly boost activity along with any surprise game or Dapp releases. Further, its gasless nature combined with ZK-rollup technology has the potential to gain market share quickly. The company has raised significant money to fuel growth, and its partnerships team has locked down agreements with upcoming games teams at an accelerated pace, so it will be worth keeping an eye on. As said by Robbie Ferguson (Co-founder / President of Immutable) - “We’ve onboarded more games this quarter (Q3 2022) than the last 2 years combined”.

- Flow is finally starting to build up a base of users beyond just collectibles thanks to the two Blitz games, Dimension X and Chainmonsters. Despite being a somewhat under-discussed blockchain, Flow is already starting to outpace WAX, Polygon, and Immutable in NFT transaction volume, which hit ~$20M by the end of Q3 2022. The Dapper wallet’s ease of use and effective fiat-to-crypto on-ramping can make a big difference as the game library grows.

- As a reminder, Cryptoslam only accounts for NFT volumes in the secondary market. Also, it only includes data on the following blockchains: Ethereum, Solana, Avalanche, Ronin, Flow, WAX, Polygon, Panini, Tezos, BSC, Theta, and Immutable.

In conclusion, the peak (~$4.5B) and floor (~$500M) of NFT transaction volume (albeit secondary market transaction volume only) over the last 12 months showcase where the space is in terms of value generated at the current state of adoption. For comparison, mobile F2P gaming is a $100B+ market and has historically grown at a respectable rate year-over-year.

Number of Blockchain Games

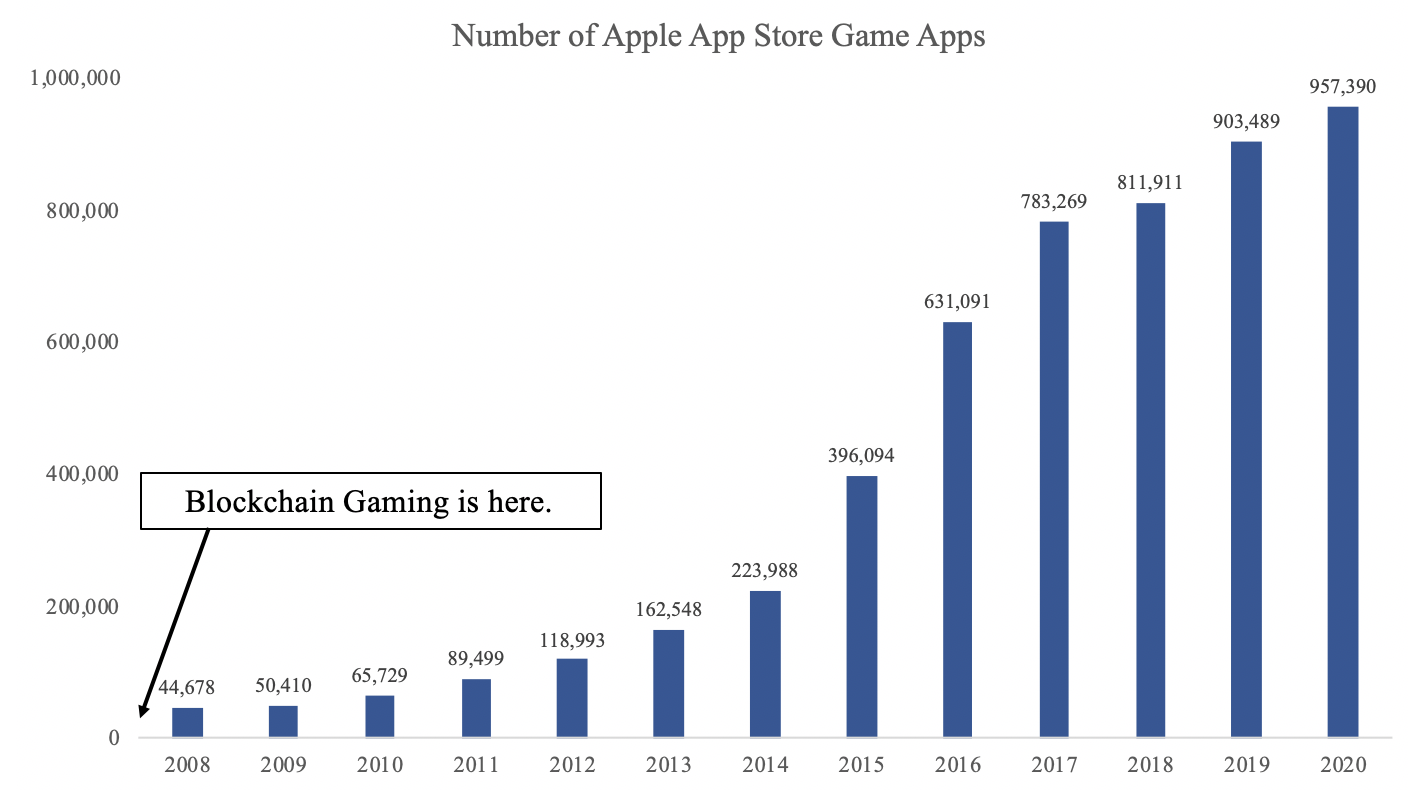

Finally, we think it’s important to highlight just how early blockchain gaming is in development. According to DappRadar, fewer than 2,000 gaming applications currently utilize the blockchain. Compare that to the tens of thousands of gaming apps in the App Store in the first couple of years after launch.

Since a game’s development cycle is typically measured in years, we expect to see many more games released over the next few quarters and years. This will be impacted by the time required to build infrastructure, development tools, distribution channels, and product design best practices. These were critical pieces for the Apple App Store and Google Play Store to get right before seeing explosive growth in the number of apps hosted. Even from this metric’s lens, blockchain gaming has quite a long way to go in actual mass adoption.

To track how blockchain games are moving towards mass adoption, check out our monthly blockchain market reports on Naavik Pro.

#2: The Fall of P2E Gaming and Market Speculation

There’s a strong bifurcation in blockchain gaming right now. The bear market continues to rage, and unsustainable, ponzinomic, and non-fun games (essentially the first era of blockchain games, namely play-to-earn games) continue to deteriorate month after month.

However, the next generation of fun games that are less dramatically play-to-earn is steadily being built by many talented teams worldwide.

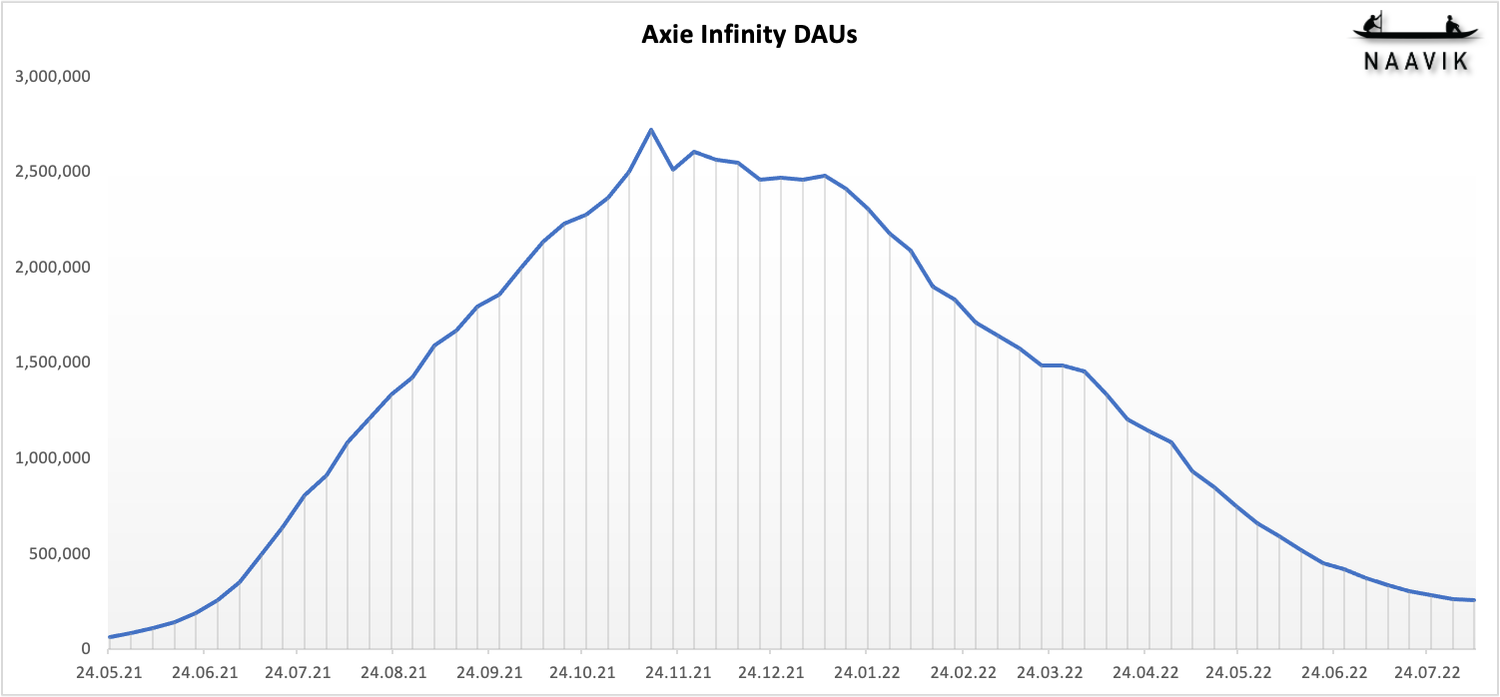

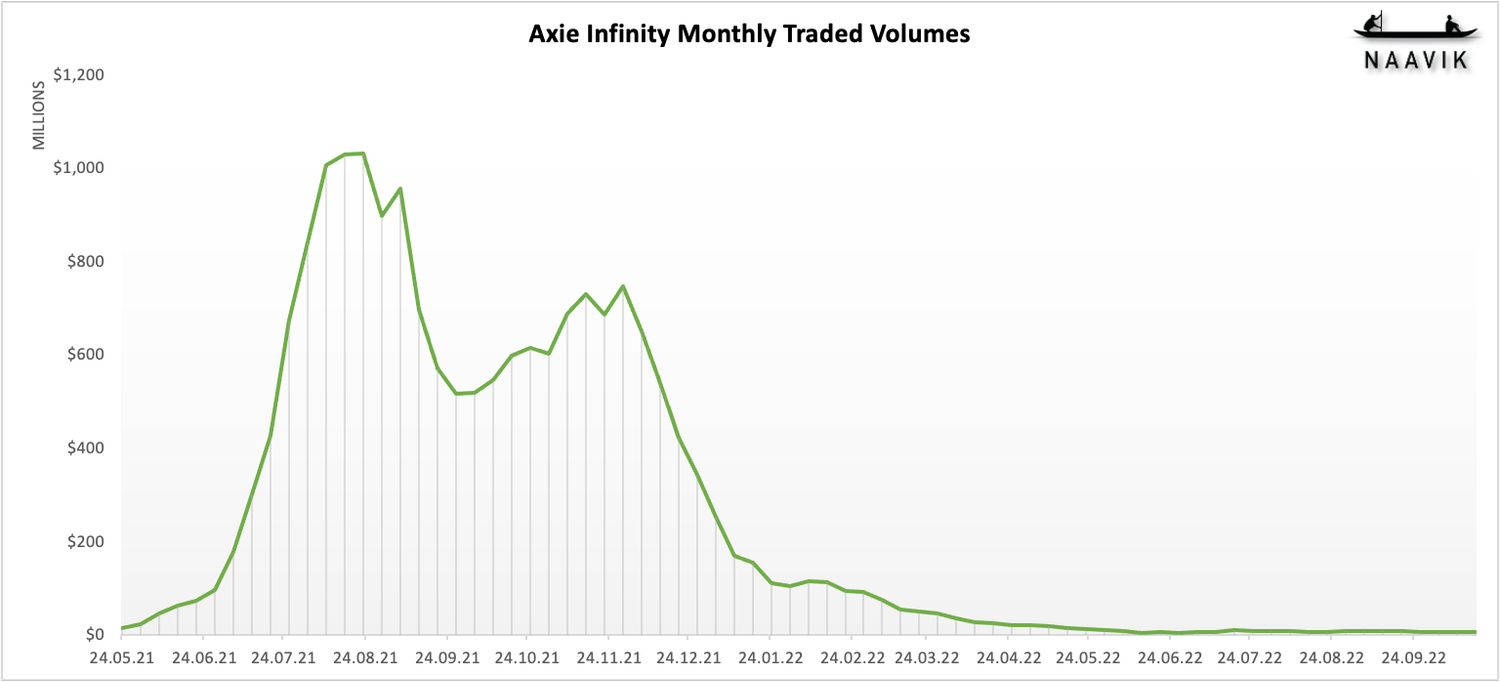

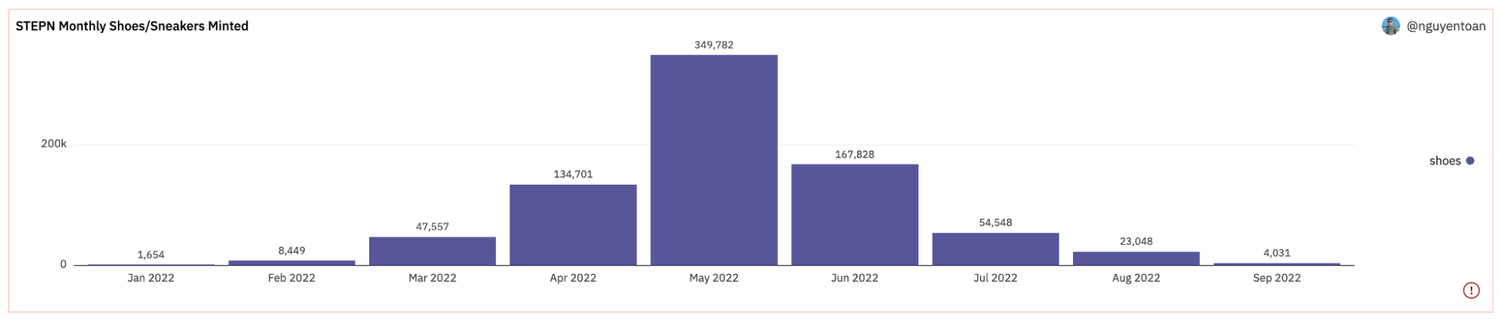

What’s challenging is that because great games take time to make, the existing games are falling apart faster than the next era of games can launch and prop up industry growth. This leads to rough-looking industry statistics. The major highlights are how the token prices of major first-era games – such as Axie Infinity, Pegaxy, Crabada, and STEPN – are all down approximately -80% and more from their peaks.

Further, these “top” games continue to shed users, as can be seen below in Axie Infinity’s user numbers taken from our Axie Infinity deconstruction:

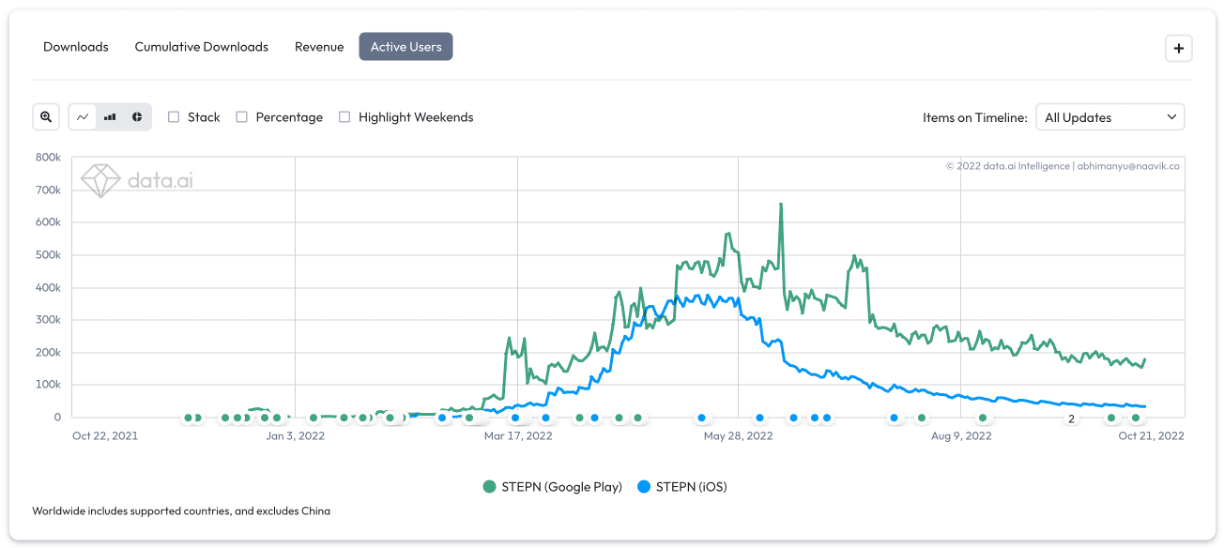

Or even STEPN for that matter, as we explored in our STEPN deconstruction:

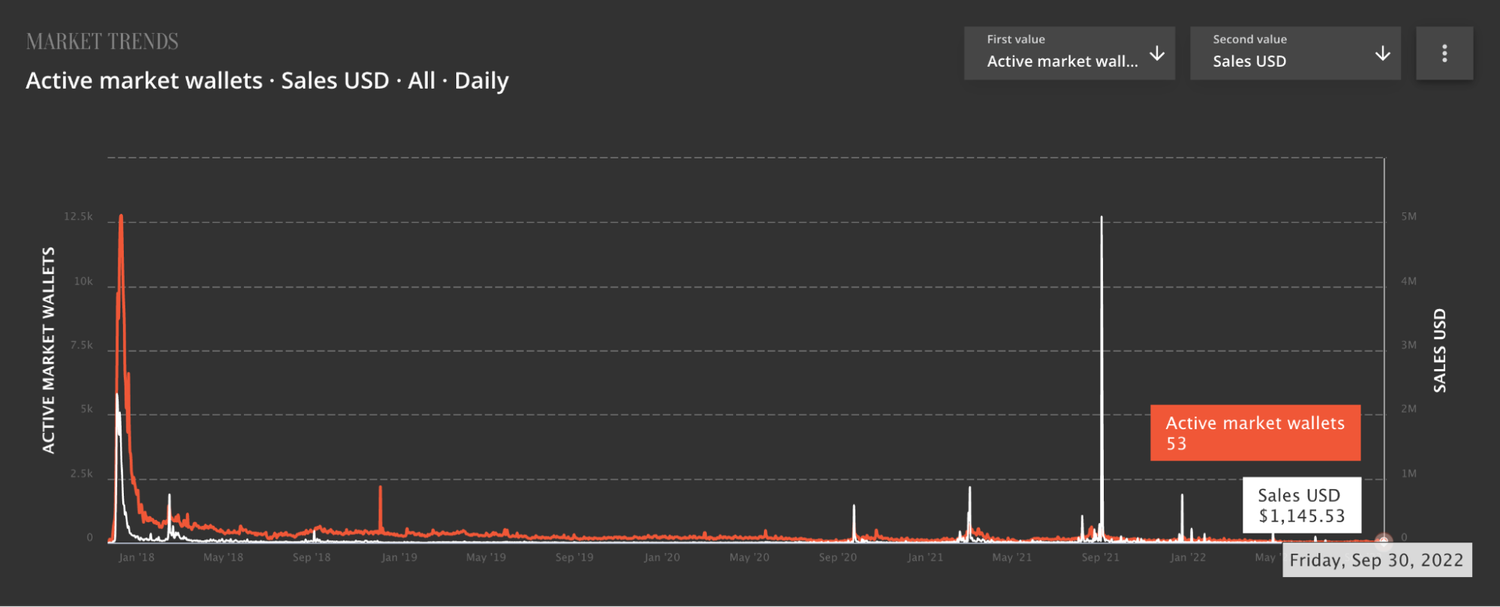

Plus, in a bear market, many retail investors/users are less willing to shell out significant money for NFTs than they were 6-12 months ago, and that eventually results in lower dollar volumes being traded across the entire space as exemplified by Axie Infinity and STEPN below:

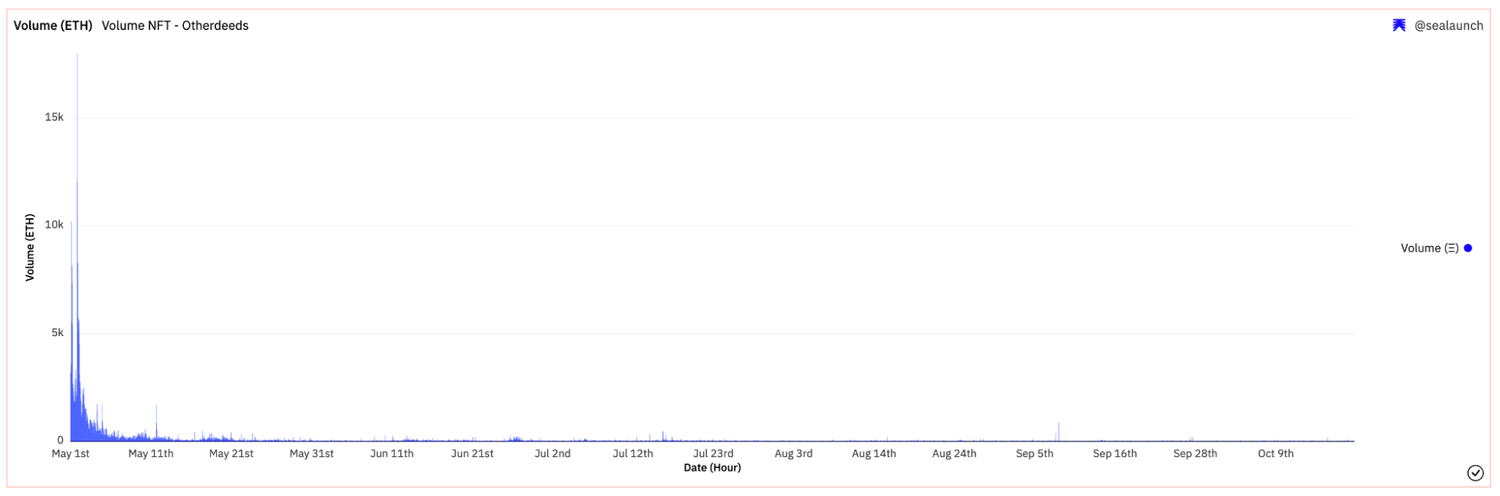

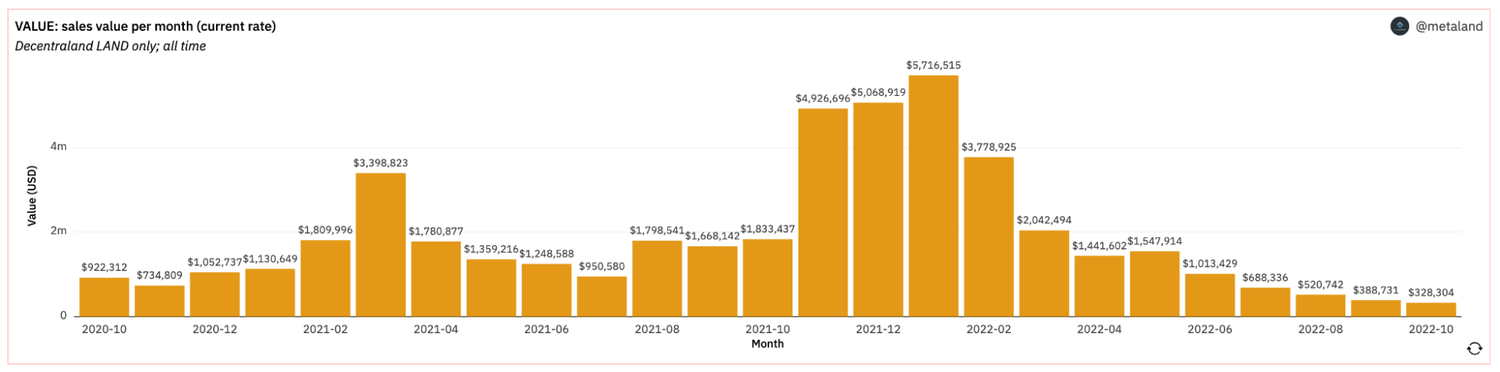

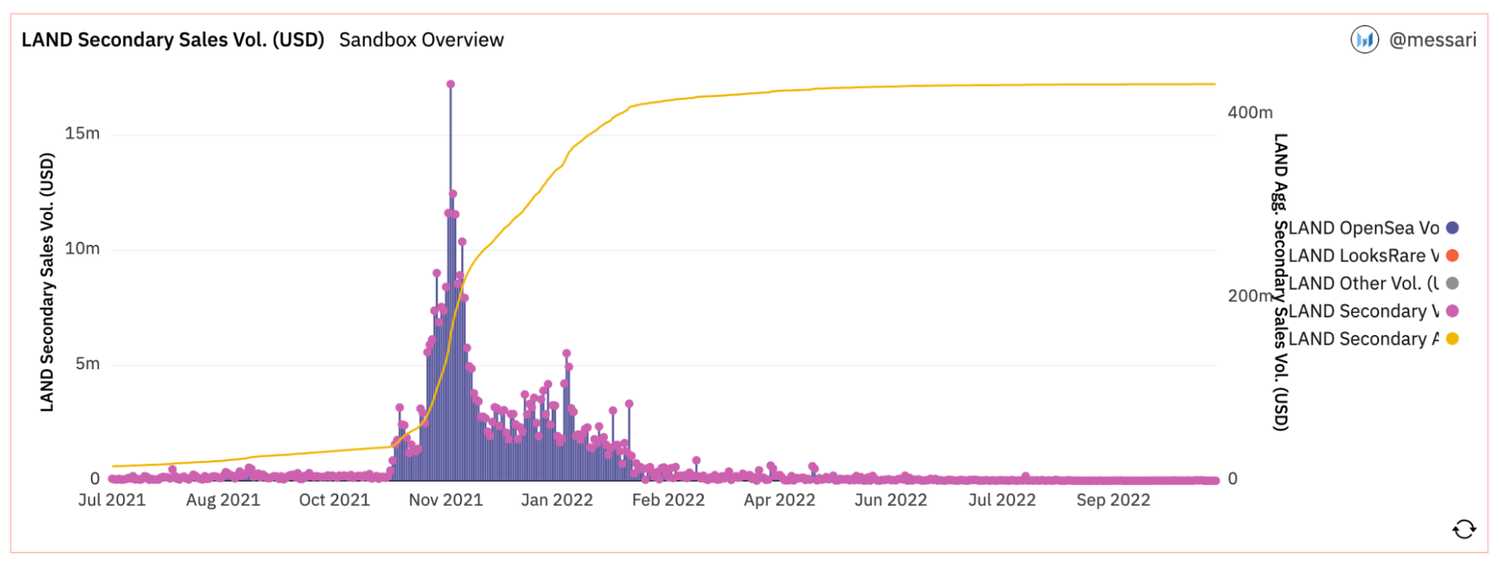

Very much related to the above, we also see similar downward trends across other speculative game-related assets – most notably virtual land NFTs belonging to games that are yet to launch. In other words, market speculation during this bear market is not where it used to be during the 2021 bull run of play-to-earn gaming. This is seen in the drop in sales volume for virtual land NFTs belonging to Yuga Labs’ Otherside, The Sandbox, and Decentraland, respectively:

In a nutshell, it’s a tough time to be a gamer, developer, or investor in the crypto space.

All that said, we continue to push what we’ve said since day one of Naavik Pro: the time will likely come. It just takes some patience, and in the meantime, we should learn all we can to best prepare for spotting future opportunities (as developers, founders, or investors).

CryptoKitties defined the first era of blockchain gaming primitives. This era showcased what NFTs and “player” ownership could mean, but (limited functionality aside) it was fundamentally held back by the Ethereum network’s complete lack of scalability (and there were no other options).

Axie Infinity defined the next era. Sky Mavis built a real game and used scalability solutions. Still, Axie Infinity’s fatal flaw was economic design — prioritizing unsustainable earning (yield) over fun, which cascaded across countless copycats and infrastructure built around it (guilds, tooling, etc.). As previously discussed, this led to a strong demise of P2E gaming across the board, such as Axie Infinity, STEPN, Thetan Arena, and Crabada, which have all lost upwards of 90% of their market capitalization over the past year.

To learn more about the inner workings of the fatal flaws in the economic design, please read our full deconstruction of Axie Infinity since this game not only pioneered a highly innovative business model but also set irrational industry standards in many ways. The blockchain game developer community is now unlearning and rebuilding new game design, economy strategy, and tokenomics best practices.

The next era of crypto games, to (over)simplify, will build off of the previous two eras — using various scalability solutions and sidestepping the most significant economic flaws while prioritizing fun. It doesn’t mean everything will be perfect, come instantaneously, or take over everything — none of that will be true — but there’s too much talent, capital, excited players, and building momentum (despite the bear) for much of this to not come to any fruition. Great teams are building, and eventually — over the next year or two — we’ll likely see the next wave of growth: catalyzing active wallets, engagement, and transactions to new highs yet again. Here are three projects that continue to impress us.

Splinterlands’ Quest for Growth

One key example that has impressed us is Splinterlands. Over a few months, Splinterlands has gone from a singular success to a series of recent explosive announcements, including selling a new PFP project, pre-sales for a new card set, developing two new games, releasing a podcast and hosting their first-ever Splinterfest convention! The pace at which the team is building its entire ecosystem and strengthening the long-term utility delivered to the community is one to applaud.

Even in terms of Splinterlands’ specific moves, the team has not let the current market condition deter them from chasing success. For example, the team began pre-sales for new card packs sold for the game’s core governance token, SPS, instead of the utility token, DEC. The sales profits also went to the DAO instead of the company, creating additional value for SPS holders rather than for Splinterlands. These changes must have been well received as all 500K packs sold out in 96 seconds for over 25M SPS and $500K in vouchers, which whales of the game own. Most interestingly, the bullish behavior didn’t end there, as 500K packs didn’t seem to be enough spend depth, and whales started rapidly buying SPS Validator Node licenses that the remaining 1,300 in the tranche sold out. This created even more value for SPS holders as 80% of the SPS spent were burned, and 20% went to the DAO, another situation where the company wasn’t making a profit.

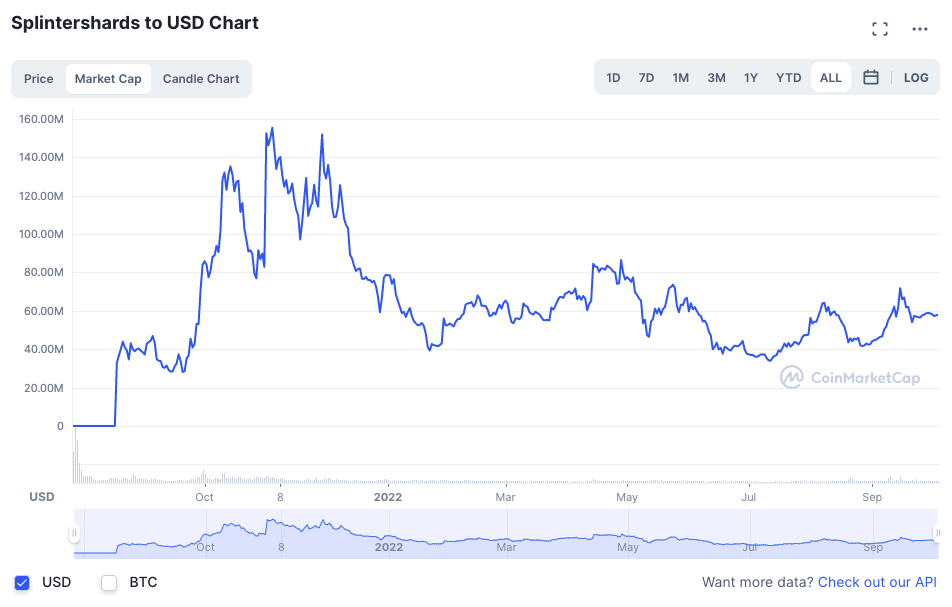

While we will keep an eye on the trajectory of its many projects over the next year, it is a team and project to gain inspiration from when it comes to wading through crypto gaming winter waters. Don’t take our word for it though — look at Splinterlands’ market capitalization graph below, which hasn’t suffered the same haemorrhage as other P2E projects over the same period. Check out our Splinterlands deconstruction to learn more.

Sorare’s Sustainable Economy

The second example is none other than Sorare, which is based in France and was developed in 2018 by Nicolas Julia and Adrien Montfort. Sorare is an Ethereum-based fantasy sports game in which players buy, sell, trade, and manage a virtual team with digital player cards. Overall, Sorare has a sustainable and arguably very profitable model, which is still rare among blockchain games.

Fantasy sports games have been massive for a long time. What raised a few eyebrows, though, was when Softbank led a $680M Series B round that valued the company at $4.3B in September 2021. This valuation can be questioned today, considering the ongoing crypto winter and broader sell-off in financial markets. Still, the high valuation indicated Sorare was potentially pioneering something big. Overall, according to Crunchbase, the company has raised $739.2M in 4 rounds to date.

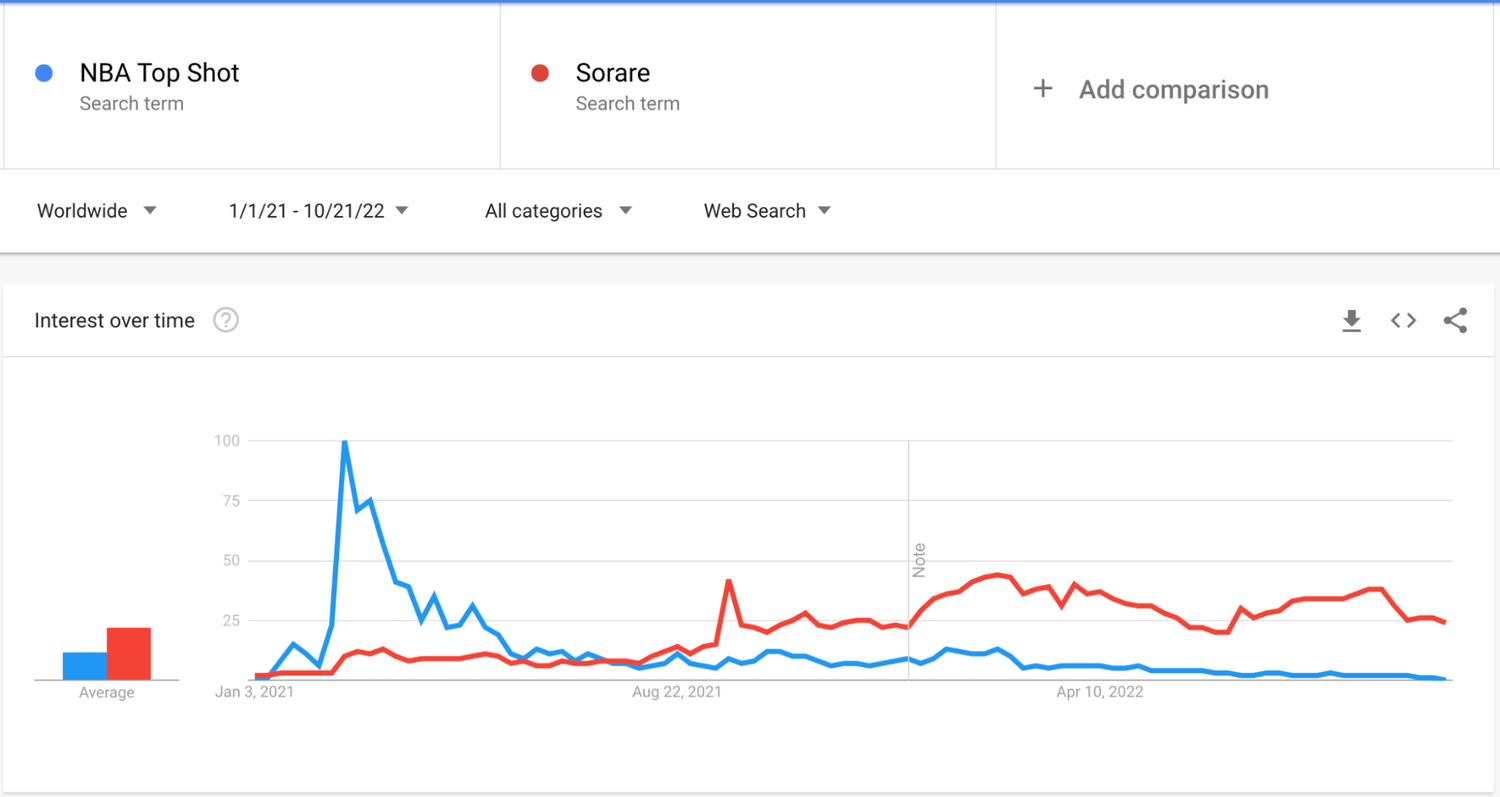

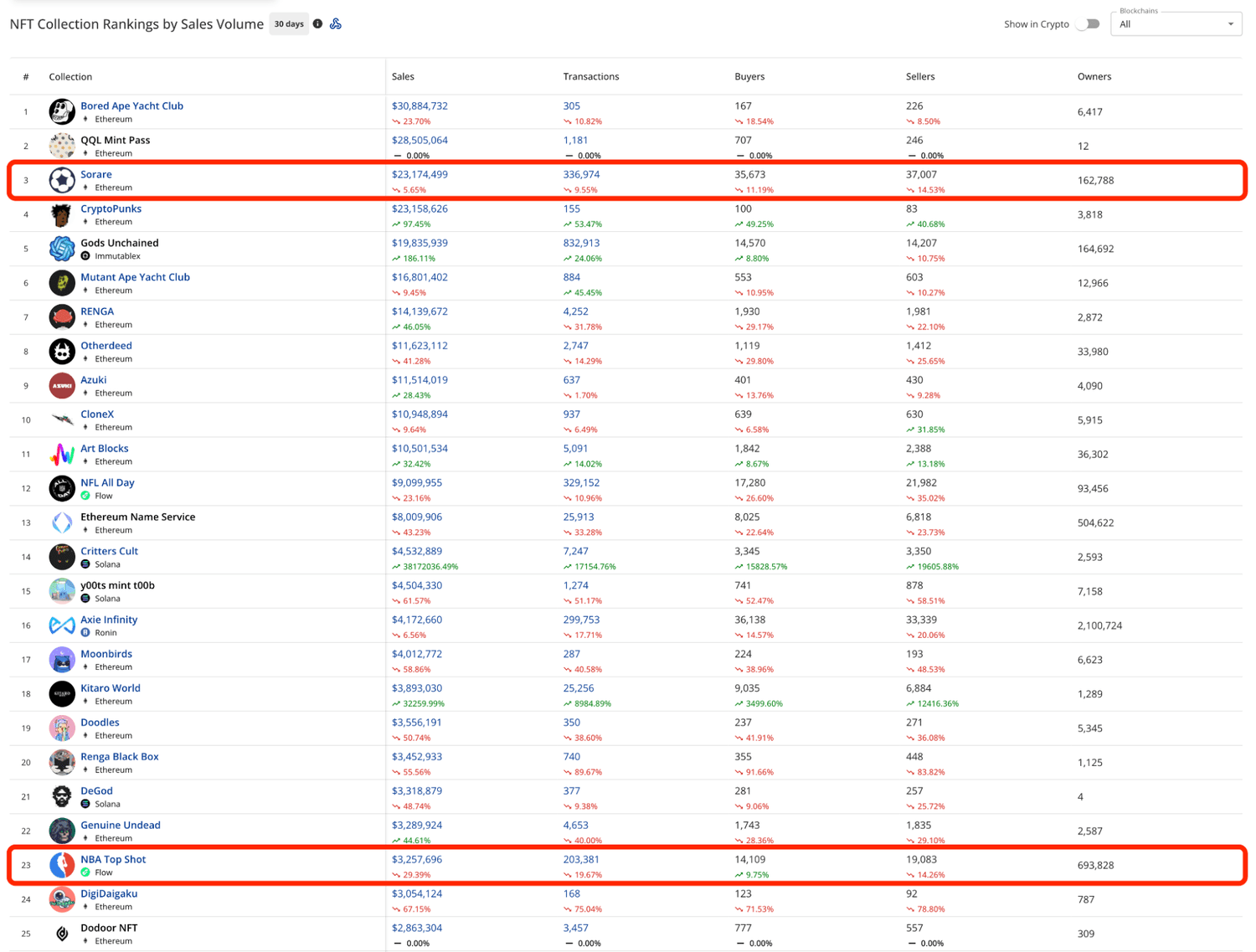

To more strongly showcase whether Sorare has been able to deliver on its vision and a sustainable business, let’s also briefly compare it to NBA Top Shot. It’s not a fantasy sports game — rather an NFT collection of top player moments — but Sorare and NBA Top Shot share the commonalities of being on-chain, sports-related, and collectible-based. With the caveat that football is more popular than basketball on a global scale, it’s worth noting how interest in these two projects (at least according to Google Trends) has changed over time.

As seen in the chart below, Top Shot rolled through the typical hype cycle seen by many crypto projects and remains well below its highs, while Sorare has seen steadier growth in interest since its launch.

Looking at the past 30 days of secondary market sales volumes (as of mid-October) among NFT projects, Sorare is ranked #3 with $23.2M, while NBA Top Shot stands at #23 with $3.3M. Of the top 10, it also has the second-highest number of buyers, which points to a relatively healthy ecosystem.

Since Sorare is a F2P game (free to start with the ability to buy or win better player cards), it has approximately 500K users who play the game. Sorare has 150K cumulative on-chain card holders, of which 30K transact monthly. Sorare differs from most fantasy sports products because users need to purchase cards of football players to play the game at a high level. Other fantasy sports usually gate the entry to the game through a dollar-based tournament entry cost or maybe F2P with ads as part of a larger ecosystem. Sorare has a fixed number of player cards to sell in a given year, and that's where it generates almost all of its revenue.

In a statement following the latest funding round, Sorare co-founder and CEO Nicolas Julia said, “We saw the immense potential that blockchain and NFTs brought to unlock a new way for football clubs, footballers, and their fans to experience a deeper connection with each other. We are thrilled by the success we have seen so far, but this is just the beginning. We believe this is a huge opportunity to create the next sports entertainment giant, bringing Sorare to more football fans and organizations, and to introduce the same proven model to other sports and sports fans worldwide.”

The team is clearly delivering! Sorare now has 170 employees, over 50 job openings, and clear expansion plans. Sorare started with fantasy football (or soccer for the Americans reading this) but has recently added baseball. Also, Sorare recently announced a collaboration with the NBA and PGA Tour to further expand into basketball and golf. This is a team and project to keep an eye on going forward. To learn more, check out our Sorare deconstruction.

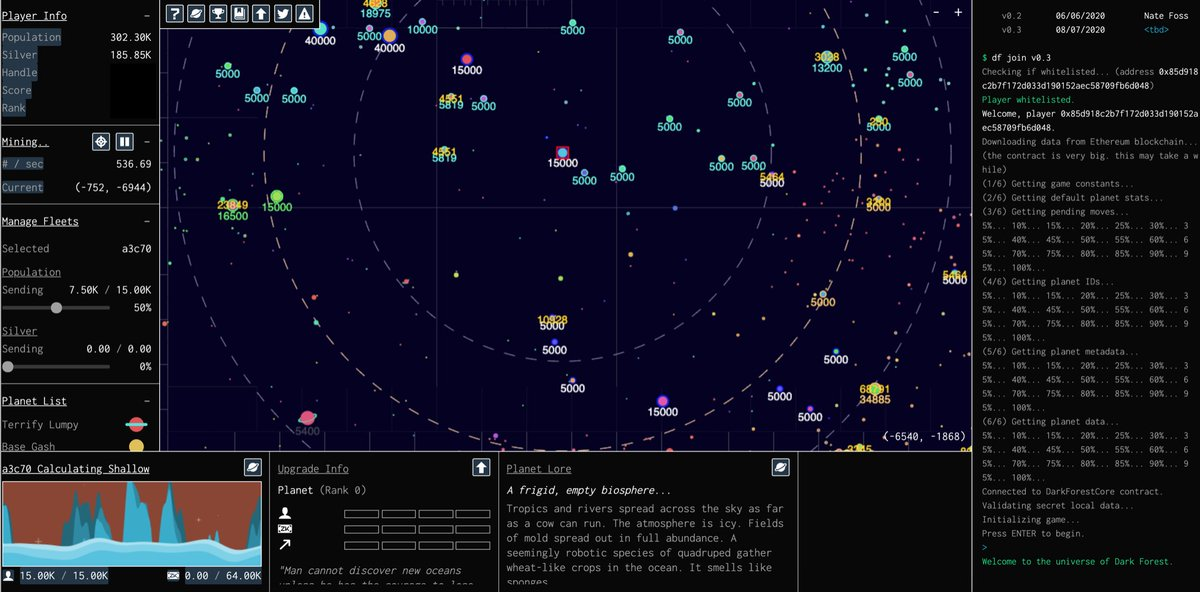

Dark Forest and Innovation in Blockchain Games

Dark Forest is a result of what started as an undergraduate project for MIT student Brian Gu, who eventually took a leave to work on it. It was envisioned as a way to explore a new set of “zero-knowledge” technologies. The Dark Forest team looks at blockchain technology differently than other blockchain gaming teams, seeing it as a vast, distributed computer that can create “credible commitments.” In other words, it is a machine with verifiable and predictable behavior and is not dependent on any private entity to continue functioning. Dark Forest is the team’s first exploration into what such a computer might be able to do.

Named after the second book in the Remembrance of Earth’s Past trilogy by Liu Cixin (more commonly known as The Three-Body Problem Trilogy), Dark Forest is a multiplayer version of the classic Flash strategy game Galcon (originally an entry in 2006’s Ludum Dare 8 with a theme of “swarms”) at its core. In Galcon, each level is a map full of planets of various sizes. Some are owned by factions (AI and player), and many are neutral. The goal is to capture/conquer the map. To do this, the player sends ships to capture other planets. Capturing planets allows you to produce more ships with which you can eventually conquer the map. It’s like Risk but in real-time and in space.

While Galcon was a fast-paced tactical game, Dark Forest recasts those mechanics as a large-scale massively-multiplayer 4X strategy game. More importantly, there are two primary technical achievements in Dark Forest that the rest of the blockchain gaming space can benefit from: first, it’s an entirely on-chain game, and second, as an on-chain game, it has secret information.

When one says a game is entirely “on-chain”, it means that it is a trustless system in which all actions in the game are submitted, verified, and recorded by the smart contract, with no centralized server processing game actions and no centralized database storing the information. There are very few genuinely on-chain games.

Furthermore and most notably, Dark Forest is one of the first blockchain game implementations of zk-SNARKs, which stands for ‘zero-knowledge succinct non-interactive argument of knowledge’. While we won’t get into the details of how zk-SNARKs work, what’s important to note is that in the case of Dark Forest, it enables the concept of on-chain “fog of war.” In other words, players can exist in a shared world and make moves verified on the blockchain yet remain hidden from other players who cannot “see” them. This is a pretty surprising capability — a player can commit a verifiably legitimate move to a public chain without revealing what the move was.

One can tell that Dark Forest has an idealistic vision of Web3 deep in its DNA. What exactly that means is up for endless debate, but the game was not created to become a billion-dollar sensation for investors to swoon over. Instead, it was built on a foundation of curiosity, discovery, exploration, and collaboration. Games like Dark Forest aren’t making headlines, but some of the most important, influential, and — yes — even profitable innovations in blockchain gaming will likely come out of projects like this. To learn more, check out our Dark Forest deconstruction.

Download the Full PDF Report

Sign up with your email address to receive the full PDF report, and sign up for Naavik Digest.Sign Up

#3: A Radically Different Funding Environment

To understand the state of today’s blockchain gaming funding environment and where it’s headed, we’d like to provide some commentary on the Q3 2022 numbers. But let’s start by rewinding to Q3 2021 funding numbers.

Blockchain Gaming Funding in Q3 2021

Back then, blockchain gaming funding was indeed on fire. Q3 2021 alone got an outstanding $1B+ deal value across 22 deals, while the cumulative Q1-Q3 2021 deal value of $1.58B represented an overwhelming 34x growth YoY and a total deal count of 50 meant a 4x jump YoY.

There was a heavy concentration in Seed rounds (~55%), but check sizes were usually small (~$3M/deal) and made up 4% of all the Q1-Q3 2021 deal value. That means investors were fine getting in early through private token sale rounds but were also cautiously skeptical. 70% of the total Q1-Q3 2021 deal value was in various Series A/B across a total of 11 deals, with the most notable being Sorare at $728M (Series A + B), Forte at $185M (Series A), Mythical Games at $75M (Series B), and Immutable at $60M (Series B). Other notable Series B+ deals included Dapper Labs’ $250M raise and Animoca Brands' ~$140M raise.

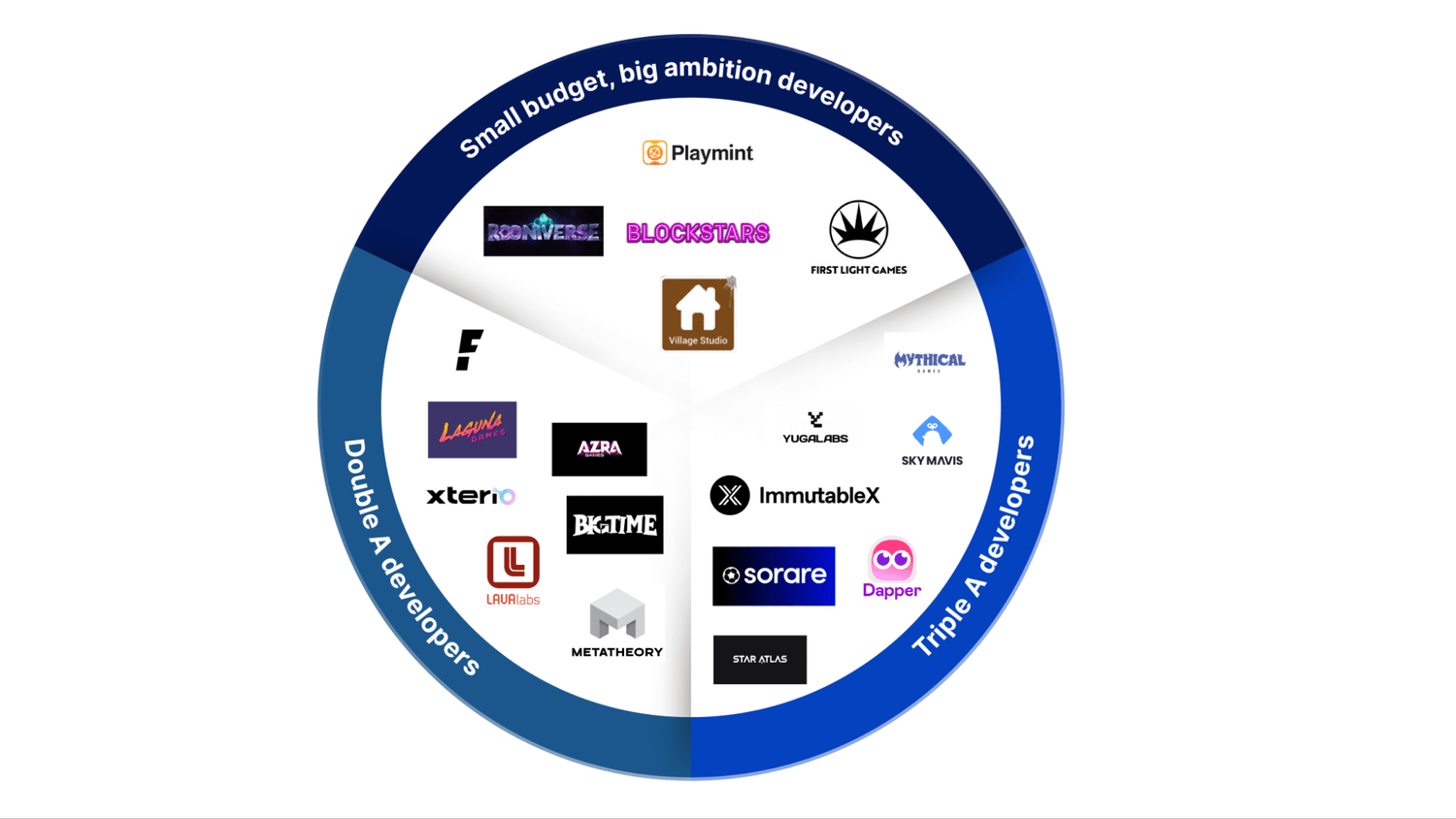

Overall, it was pretty clear in Q3 2021 that the companies commanding the most significant funding rounds were the ones who seized the moment to build platform layers on which the future of blockchain games could live. Companies purely focused on building blockchain gaming content were getting significant attention too, but check sizes were much smaller. In other words, the picks and shovels of blockchain gaming got a lot of money back then. But if everyone focuses on picks and shovels, blockchain gaming would never strike gold. This is where we could see three different classes of blockchain gaming content companies already emerging — or in other words, the first AAA blockchain game developers started to bubble up:

- Small budget, big ambition developers: Rooniverse, Playmint, First Light Games, Blockstars, Village Studio, Genopets, Galaxy Fight Club, Crypto Raiders, Gallium Studios, Heroes of Mavia, Horizon Blockchain Games, Lucky Kat Studios, etc.

- Double A developers: Laguna Games, Xterio, Big Time Studios, Faraway, Azra Games, Metatheory, LavaLabs, Upland, Sipher, Illuvium, Gunzilla Games, Klang Games, Playful Studios, Iskra, Joyride Games, Gameplay Galaxy, etc.

- Triple A developers: Mythical Games, Star Atlas, Immutable, Sky Mavis, Sorare, Yuga Labs, Dapper Labs, The Sandbox, Animoca Brands, Limit Break, etc.

Blockchain Gaming Funding in Q3 2022

The funding deals data in the following report was collected in collaboration with InvestGame.

Fast forward to Q3 2022, and the funding environment looks radically different. This is the first quarter where blockchain gaming has seen negative YoY growth metrics. While the Q3 2022 total deal number was up 2.6x YoY (58 vs 22), the total deal value was down -19% YoY ($875M vs $1.1B). The QoQ growth metrics were also down, indicating the continuation of the 2022 market correction that we began to see at the start of 2022.

Over Q3 2022, ~69% of the deal count and ~36% of the deal value was concentrated in Seed round investments. Series A rounds made up for ~14% of the deal count and ~20% of the deal value. Series B+ rounds made up 5% of the deal count and 38% of the deal value. Overall, these statistics mainly showcase smaller Seed round check sizes over the year ($7M in Q3’22 vs $12M in Q1’22), 2021’s Seed round companies graduating to Series A rounds (with an average check size of $20-25M), and some to Series B/B+, as highlighted previously.

Around 1/3 of all Seed round deals were higher than the ~$7M/deal average, with Animoca Brands Japan, Klang Games, Xterio, and Meta World seeing Seed check sizes ≥$30M. Almost all Series A deals (8) were higher than $10M/deal, with Gunzilla Games, Iskra, and Planetarium Labs seeing Series A check sizes ≥$30M. The remainder deal value of the quarter was in various Series B+ rounds across a total of 3 deals. The biggest Q3 2022 deals were Limit Break’s $200M raise and Animoca Brands’ $110M raise.

One investment that definitely skews the overall deal data is the ex-Machine Zone (MZ) team’s Limit Break’s $200M raise at a reported $1.8B valuation and from a suite of investors like Paradigm, Standard Crypto, Buckley Ventures, Coinbase, FTX, and Anthos participating. For context, MZ previously sold to AppLovin back in 2020. It’s not every day we hear about $200M pre-launch raises, but there’s something here to be excited about, which we will dig into later in the report. MZ pioneered new ways to engage and monetize whales, and the new web3 paradigm allows gaming to continue to push the boundaries on what it means to have whales as both owners and key determinants to inflation, gameplay, and monetization.

Overall, it seems like the blockchain gaming deal market continues to mature into its next stage. The companies garnering most of the funding attention are no longer the ones building platform layers on which future blockchain games could live, but rather the blockchain gaming studios that can produce engaging content that uses blockchain gaming infrastructure. This doesn’t mean that investors have lost their appetite for infrastructure companies, but just that there aren’t too many more infrastructure opportunities hitting the market. Lines have likely been drawn in the sand across current infrastructure competitors, and the fight for market share has begun.

All that said, both the deal number and the deal value have further slowed down over the last quarter. And if Q3’22 performance is any indicator, deal activity will continue to normalize to realistic levels over 2022 and going into 2023. Crypto winter continues to perform a massive market cleanup, and investors are getting smarter with their bets while builders continue to build.

A Brief Note on Guilds

One class of investments that this quarter did not see much of is guilds because if there is one corner of web3 gaming under major fire, it is probably guilds. Most first-wave crypto games were built for a speculation-driven bull market, and a large majority of guilds mainly focused on Axie Infinity. Guilds also leveraged the game’s success to raise significant capital (~$200M) from VCs in the past two years with prestigious firms, such as a16z, participating in funding rounds.

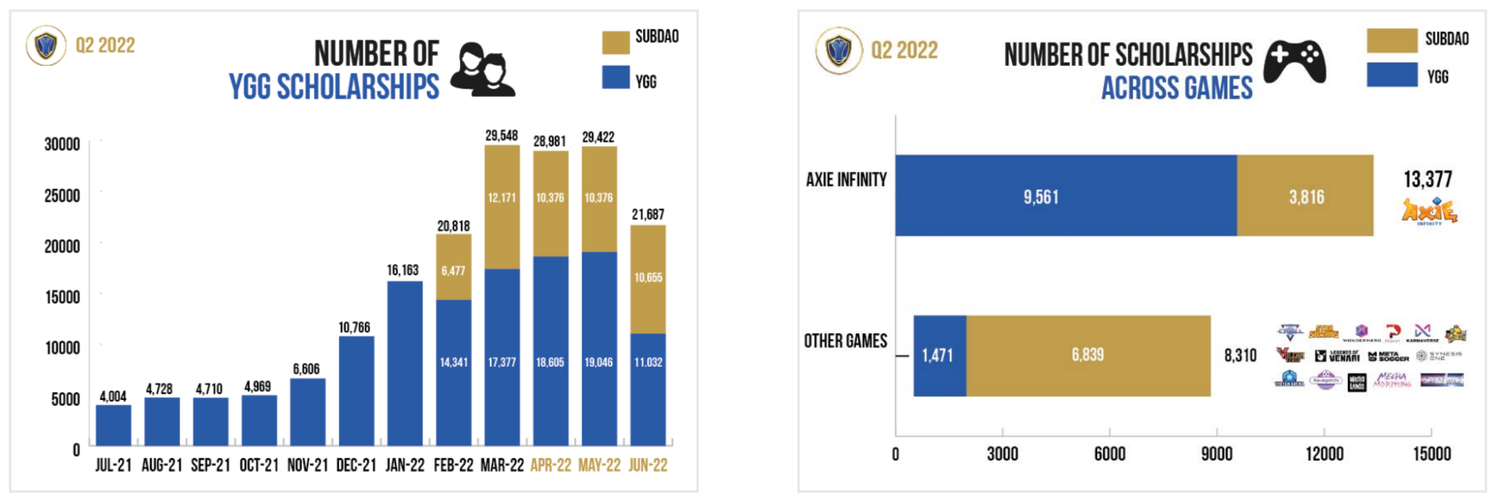

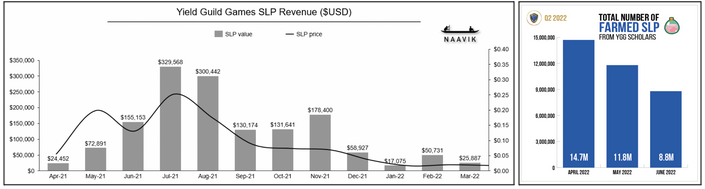

That said, guilds existed primarily to earn yield on in-game assets (while sharing the proceeds with participants, usually in developing countries). This theoretically only works in P2E games, but if P2E games are fundamentally broken and unsustainable, so are the guilds that buy-in. For super guilds, such as Yield Guild Games, not only has that led to falling new scholar numbers but also dropping distributable revenue to scholars, as seen below.

Today, and as we discussed before, nearly all of the first-wave blockchain games have been in downward spirals, which means most guilds don’t have a valid reason to exist. The buzzword for almost every guild currently is ‘pivot’, and it will be interesting to see how the seemingly bleak future of guilds plays out throughout 2022–23. Below are our expanded thoughts on the same.

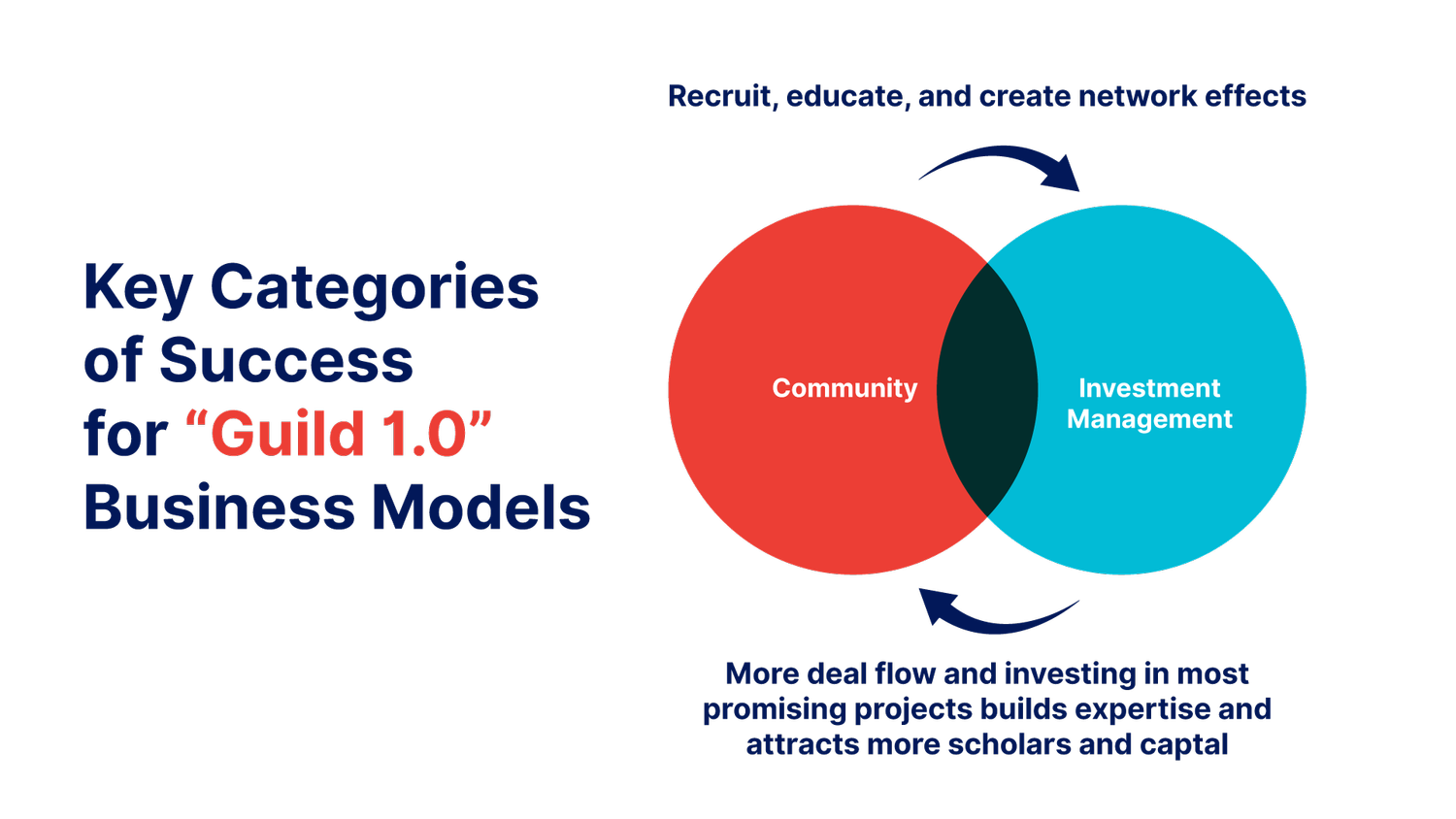

In our opinion, the “first generation” of guilds relied on two broad categories to build their businesses:

- Community:

- Recruiting, educating, and training scholars (who they rent NFTs to in exchange for a cut of earnings) to play blockchain games;

- Building social connectivity between scholars and the broader ecosystem;

- Leveraging a large network of scholars to attract entrepreneurs and gain favorable allocations into the most promising projects’ NFTs/tokens.

- Investment Management:

- Analyzing and identifying the most promising projects;

- Winning allocation of NFTs or tokens or equity at favorable terms;

- Efficiently managing scholars to generate attractive yields on these NFTs/tokens;

- Selling NFTs/tokens when warranted to earn a profitable return on investment.

With the fall of P2E gaming and market speculation, guilds desperately need to evolve to build sustainable long-term businesses and prevent themselves from going under. It is also imperative to note that thousands of guilds exist with varying degrees of size and sophistication. According to BlockchainSpace, there are ~24K guilds.

Let’s break that out into small (1-100 scholars), medium (100-1,000 scholars) and large (1,000+ scholars) size guilds to understand the spread better. According to a study performed by BlockchainSpace in March 2022: “Our guild partners represent the entire play-to-earn space, consisting of micro guilds (10–100 players; 97% of the total market), medium guilds (100–1,000 players; 2% of the total market), and macro guilds (1,000+ players; 1% of the market) covering strategically prioritized locations across the globe.” We don’t think there is any major reason to believe that this percentage split has significantly changed since then.

It is important to consider this spread when evaluating the future of guilds because there is a massive difference between the micro-guilds and super guilds (macro guilds) in terms of access to capital, in-house talent, market know-how, and organizational sophistication. And if super guilds themselves are facing a hard time in today’s market conditions, one can imagine the situation the micro and medium guilds are currently in.

For example and from YGG’s last community update: “The guild’s cash reserves will primarily be used for investment opportunities and as a runway for operational costs. YGG is putting new parameters in place to assess these opportunities and ensure that every dollar spent is in line with the guild’s strategies as articulated by its community.

Another focus is to review all cost centers to ensure that they serve both the short- and long-term strategies of YGG, with the aim of maintaining a minimum of 20 months of cash flow runway for the guild’s operational costs.

Due to market fluctuation, YGG’s total partnership value dropped 45% in Q2. To mitigate risks around the drop, the guild sold 3% worth of its asset value (US$1.3 million) to spend on operational costs, test new ways to generate funds and make new acquisitions. The decrease in partnership value is consistent with the overall market pullback, with the total market cap of crypto declining by 58% in the same period.”

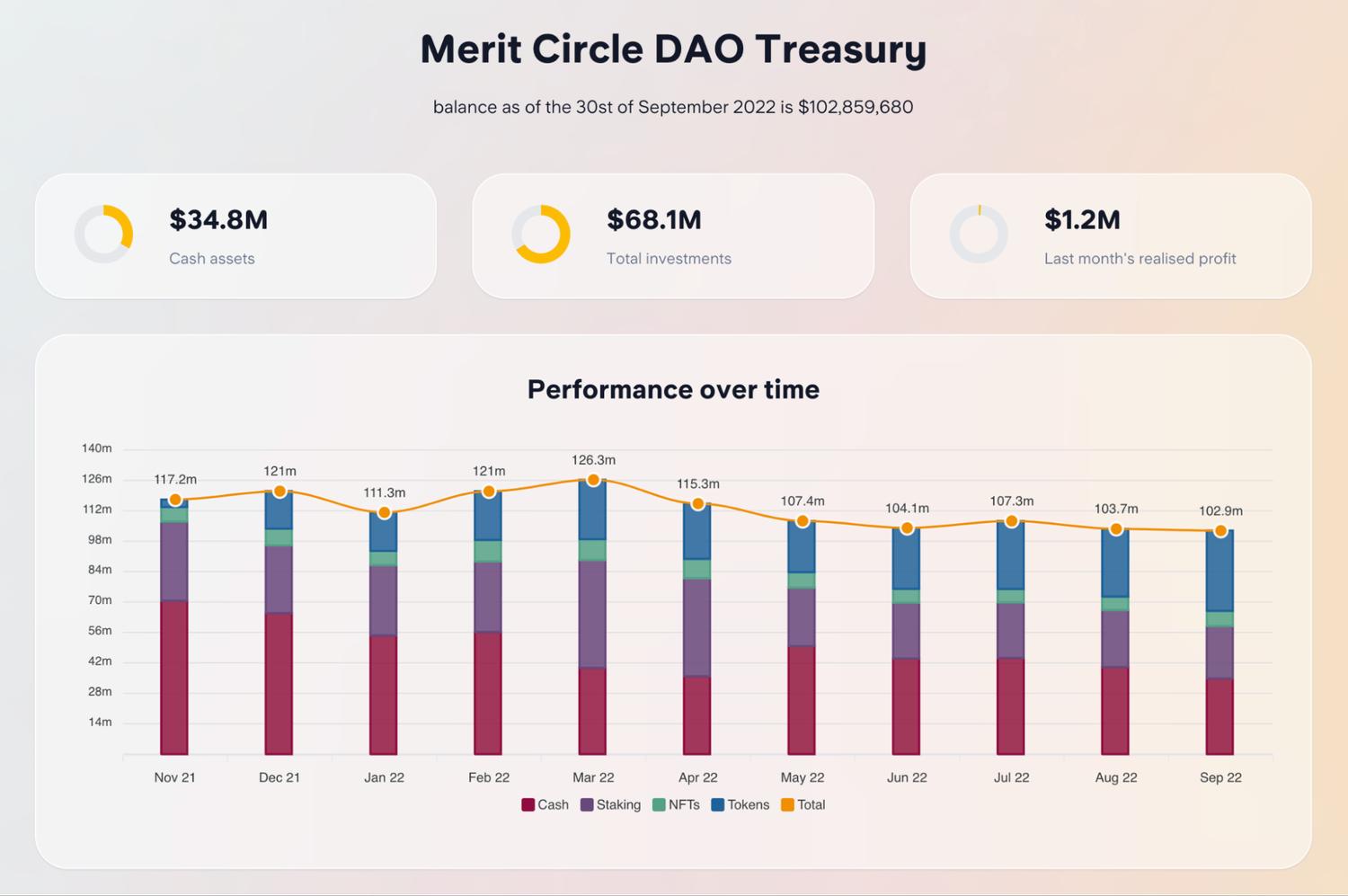

Similarly and from Merit Circle’s last treasury update: “In the past month the treasury decreased from $107,328,764 in July to $103,696,823 at the end of August, a 3,3% decrease from the previous month. The DAO realized a profit of $3,327,539$ in the month of August.”

Therefore, it is not entirely outside the realm of possibility to think that it is these super guilds (the top 1% of the market including guilds like YGG and Merit Circle) that will have a better shot at pivoting into long-term sustainable businesses versus the remaining 99% – although perhaps at lower a scale than was originally anticipated. “Sustainable” really is the key word here since it will be top of mind for the super guilds, given the past world they’re coming from.

So where do guilds go from here? There are two major paths:

- Reusing existing strengths to sustain: This mainly includes guilds doubling down on the Community and Investment Management categories previously discussed and rethinking how they utilize the headway they’ve already made there to build out more sustainable businesses. For example, YGG is increasingly moving toward becoming an esports organization with various initiatives such as the Guild Advancement Program, YGG Esports’ Elite and Rising Stars teams, and the Web3 Metaversity educational platform. YGG also continues to invest their cash balance into interesting opportunities, as previously highlighted.

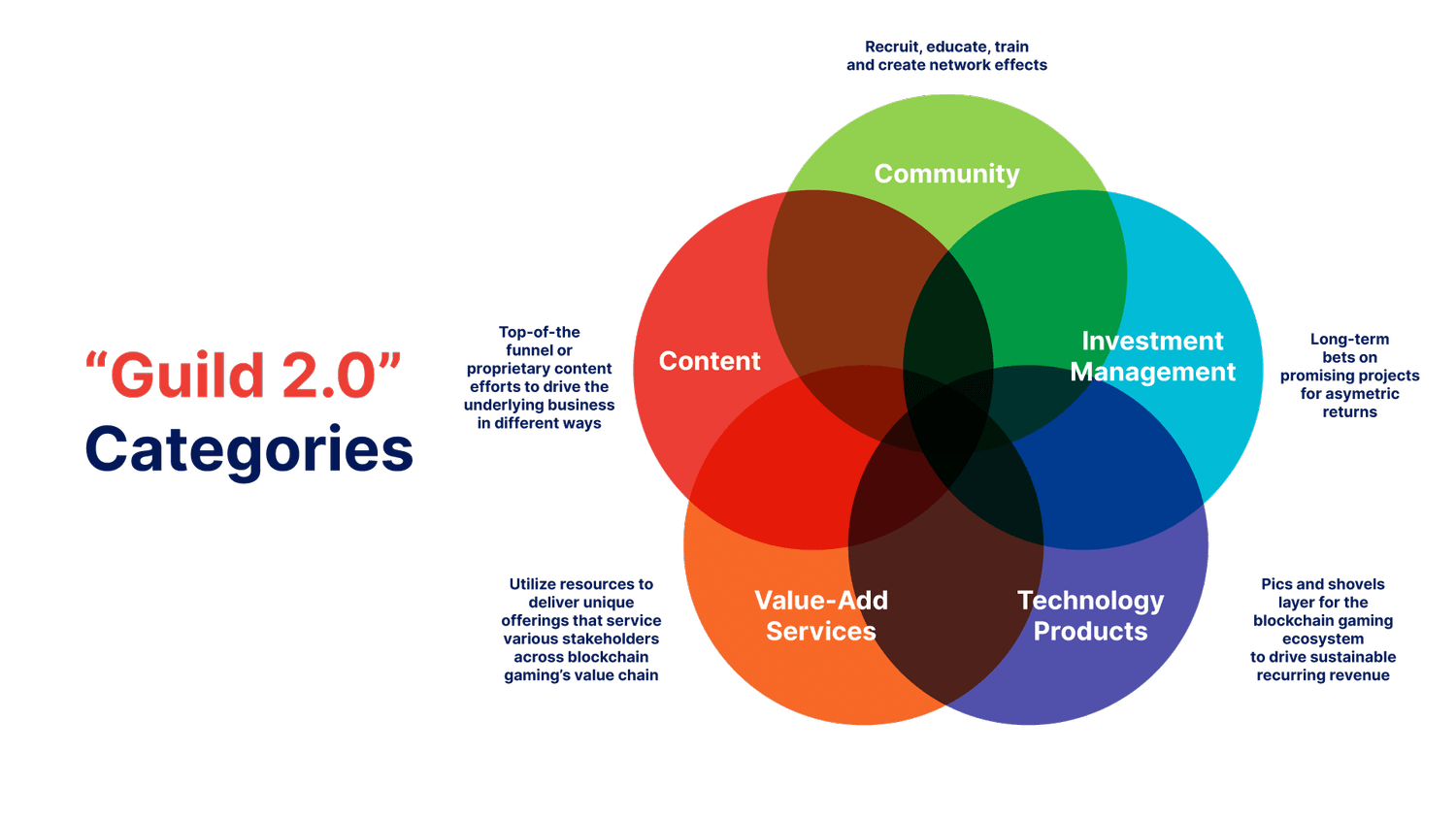

- Building new strengths to evolve: For the foreseeable future, we see three new categories of activities that will be added up to the previously showcased Guild 1.0 business model. These would be:

- Technology Products: When thinking about building a sustainable business in a gaming vertical as nascent as blockchain gaming, creating the technological picks and shovels layers is a great direction – and investors continue to look for promising opportunities here. For example, Merit Circle is moving forward with its NFT marketplace (Sphere) to compete against the likes of OpenSea. GuildFi is building out its GuildFi ID layer to allow players to access and track their in-game progress across various blockchain games. BreederDAO (although not technically a guild) is also expanding its blockchain gaming data analytics offering Playcore.

- Value-Add Services: These could come in many forms, but the general focus would be to utilize new/existing resources to deliver unique offerings that service various stakeholders in the blockchain gaming value chain and thereby support the growth of the broader blockchain gaming ecosystem. One example would be putting the lower-skilled scholar base to work by forming teams of beta-testers that provide games valuable early feedback during development. Another example would be reinvesting a guild’s blockchain gaming know-how to provide game developers with blockchain best practices, such as smart contract auditing and legal opinions.

- Content: This would include various top-of-the-funnel style content efforts (articles, game guides, podcasts, Twitch streams, TikTok videos etc.) that drive the underlying business in different ways. In the future, though, this could also include developing and publishing game content where guilds reutilise their Community, Technology Products and Value-Add Services to improve chances of success. But this will also be a high-risk strategy that only a few guilds might pursue.

It should be noted that guilds (especially super guilds) can use their cash balances to make “build or buy” decisions when exploring one or more of the abovementioned categories. M&A especially can help guilds go after ideas and verticals they don’t immediately have the talent, knowledge, or infrastructure for.

Please take the above with a pinch of salt as it wouldn’t be prudent to be overly definitive about the future of guilds in such a fast-changing environment like blockchain games. That said, the above Guild 2.0 evolution categories are based on the new ways that today’s super guilds are thinking about building their long-term competitive advantages and sustainable business futures. It also brings into question whether we should even call them “guilds” in the future. Regardless, these evolutions shouldn’t be ignored, and it is safe to assume that many micro and medium guilds will follow in the footsteps of super guilds in their unique ways. That said, it might be smart for the latter group to either focus on less versus more, or move on to new opportunities.

#4: New Frontiers and the Path Forward

By now, it must be relatively clear that blockchain gaming has come a long way since its first era, despite its ups and downs. Most notably, blockchain gaming is crucial in pushing the entire crypto space forward and to newer heights. Regarding where the future of blockchain gaming is headed, there are five key areas to keep an eye on:

- Infrastructure

- Distribution

- Talent

- Games / Products

- Regulation

Wallets as a Key Infrastructure Unlock

Of all the infrastructure solutions out there, the one that will truly unlock mass adoption of blockchain gaming (besides the blockchains themselves and perhaps marketplaces) will be the one that is closest to the players and the one that players care about the most: wallets.

Blockchain wallets were created as a better way to manage private keys and perform blockchain transactions. There are a few different types of wallets, but two relevant types are: Custodial (like Coinbase Wallet and Gemini) and Non-custodial, with Metamask being the main example. While the latter has worked well so far, many issues arise from how Metamask functions:

- First, managing private keys is still complicated and risky. Users need to back up both their private key seed phrases and their Metamask passwords because these are stored only on their computers, and if broken or lost, access to their wallets disappears forever.

- Second, Metamask functions as a browser extension, which works fine on desktop or laptop computers but is problematic when applied to mobile browsers.

- Third, Metamask is not very user-friendly, even though this has slowly improved over time; useful features like token swapping and fiat on-ramps are often severely delayed or never released.

In other words — not only are there major onboarding UX issues to be addressed, but also the complete obfuscation of the blockchain layer in the wallet experience is becoming increasingly important to solve to fuel mass adoption. While there has been a lot of interesting progress in the space (Coinbase’s non-custodial wallet, Solana’s Phantom wallet, L2s having their own wallets that connect to others etc.), there are two companies on our radar that made significant progress over Q3 2022 and are worth keeping an eye on.

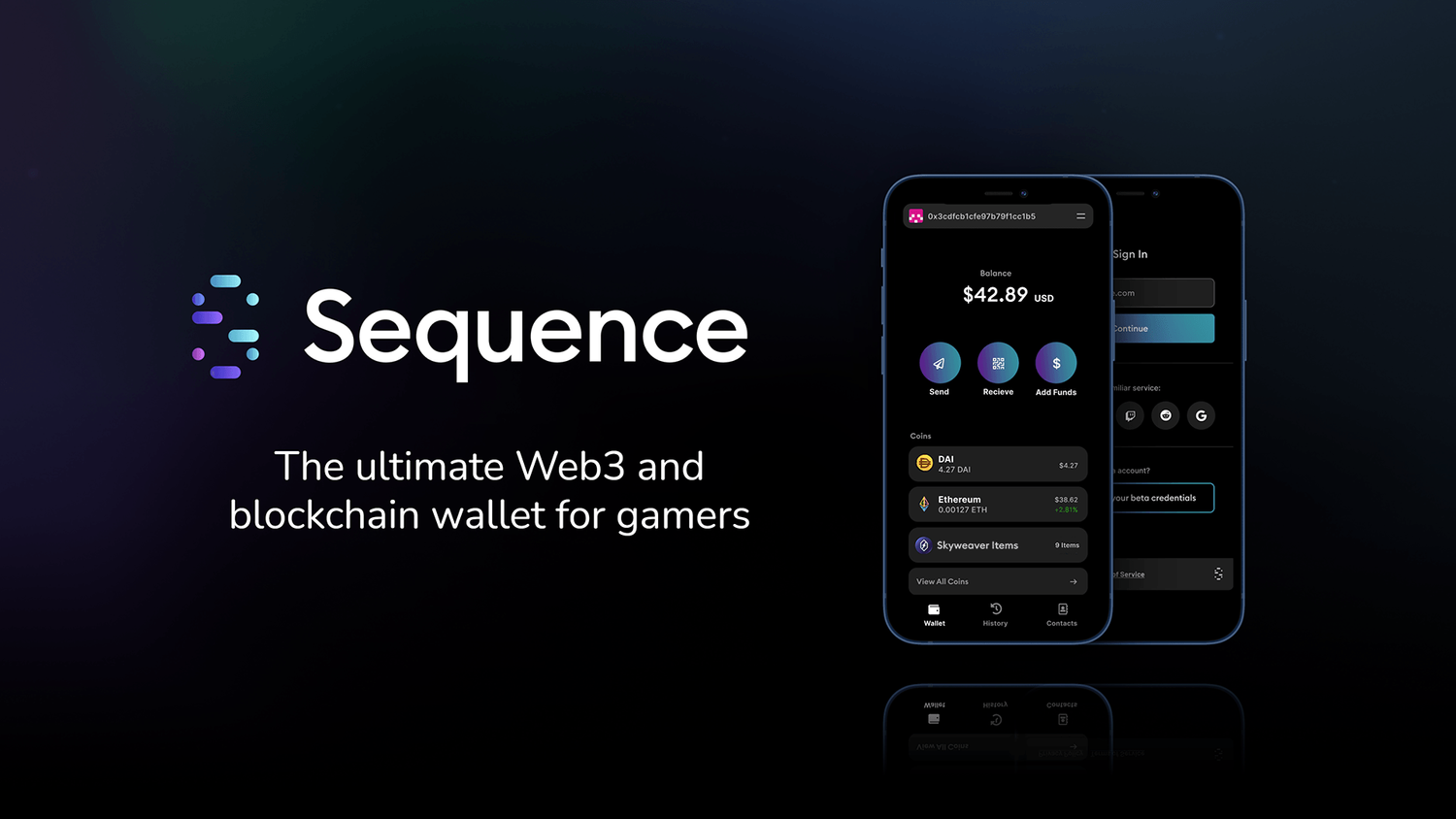

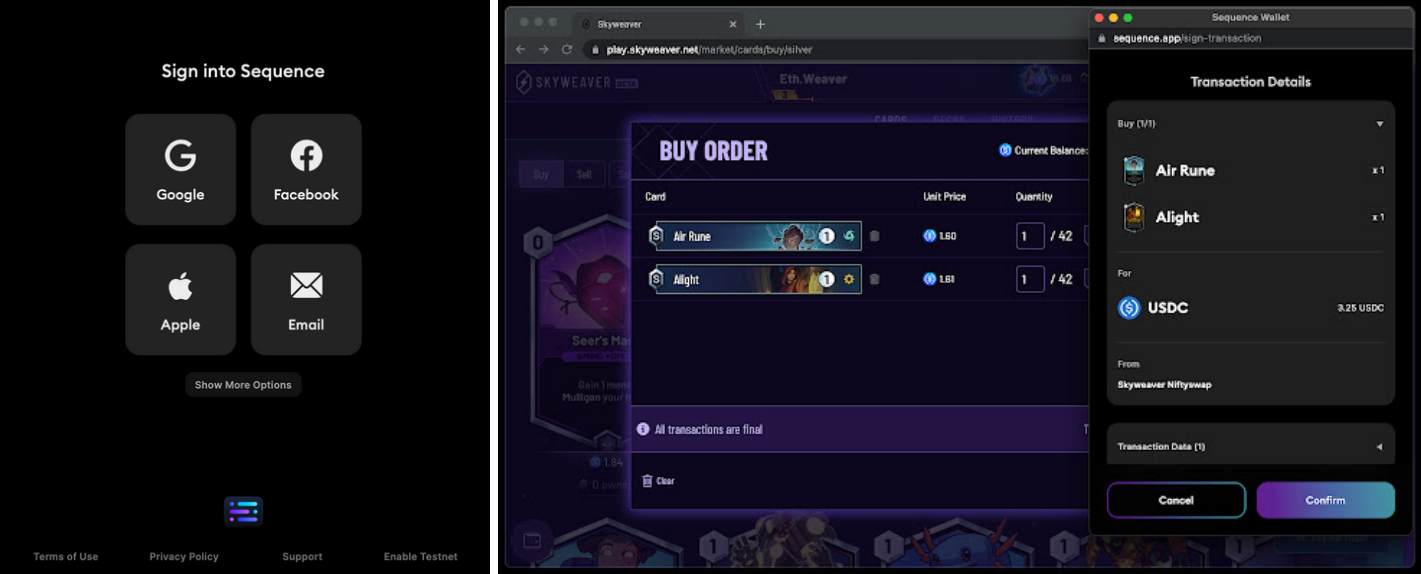

The first is Sequence from Horizon. Horizon recently raised a $40M Series A to help expand its user-friendly Sequence wallet and proof-of-concept game Skyweaver. While Metamask is the wallet that most people think of when it comes to web3, Horizon has been quietly building a major competitor in Sequence. The wallet onboarding experience could be considered as one of the smoothest and most frictionless in the market.

Horizon was formed in 2017 to create Sequence (a wallet that solves many of the problems mentioned above with Metamask) and Skyweaver (a game that uses that wallet). Much like Metamask, Sequence is a multi-chain wallet and is non-custodial but with enhanced security through its multi-key support and functionality for paying gas fees in the user's token of choice. Further, Sequence aims to be user-friendly by being a web app allowing token swaps, network switches, NFT viewing, and supporting multiple fiat on-ramps like Ramp, Moonpay, and Wyre. Finally, Sequence has been working for Skyweaver on mobile for at least a year while in beta. This has set the stage for mobile support and gives it an advantage over other games trying to use external wallet apps like Metamask or forcing players to link and manage wallets on their PCs.

Despite all this, the primary use case for Sequence so far has been as a wallet for Skyweaver to transact in USDC on Polygon. Therefore, it does need to be proven on a larger scale and across many more games. Furthermore, the needs of blockchain game developers and players will change over time, and it will be interesting to see how the wallet experience adapts.

Horizon is taking advantage of the $40M raised by launching several expansions, such as partnering with many games to support Sequence, including Sunflower Land, Metalcore, Cyball, Ethernia, Boomland, and more. This is a critical move on the company’s part, taking its polished system and getting traction as something more than just a “Skyweaver wallet.” Further, they plan to support all major EVM-compatible chains, including newer Layer 2s like Arbitrum and Optimism. It also plans to attract more developers to its platform, which should be especially interesting for mobile games looking to add web3 with fewer wallet headaches. Accelerating support for developers allows them to focus on the game element and lets Horizon handle web3 interactions across any EVM chain (leaving Solana developers a little out of luck for now).

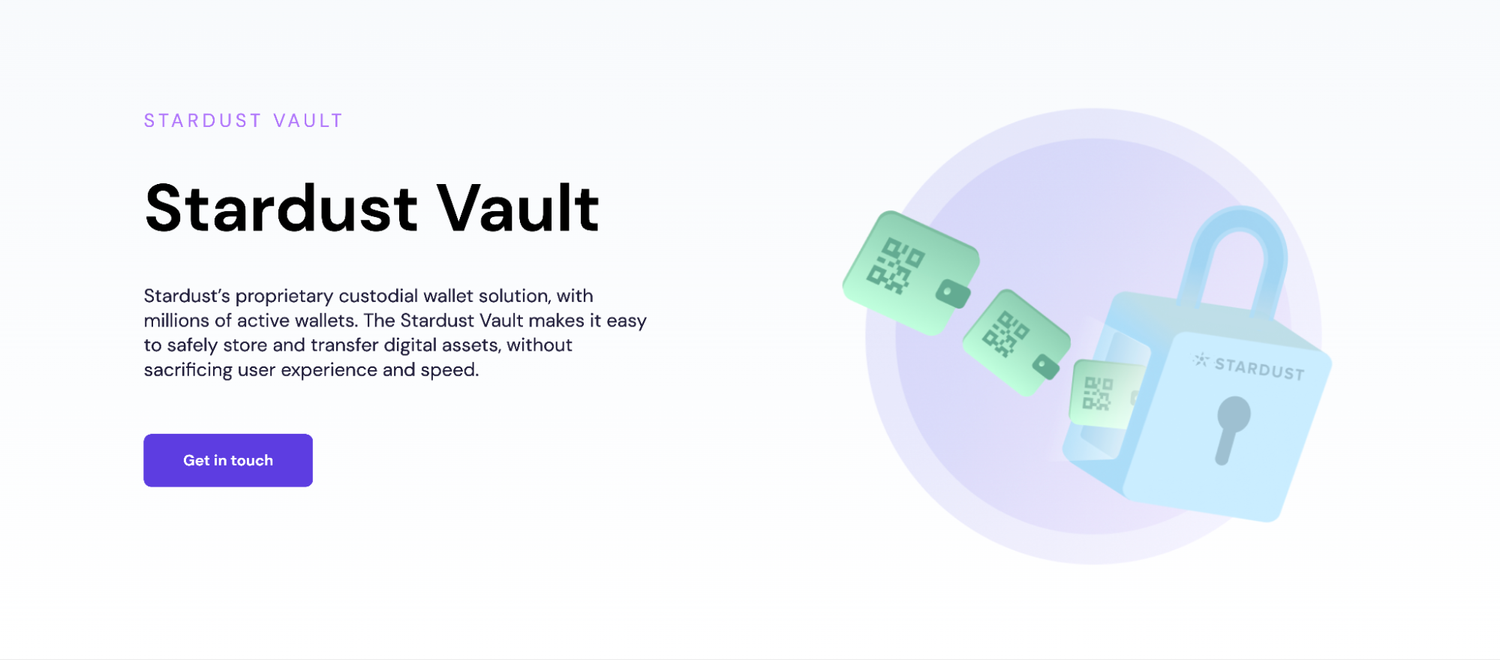

The second company to keep an eye on is Stardust, which recently raised a $30M Series A. Stardust provides on-demand web3 services to game developers in the form of APIs that can be quickly and easily leveraged. These APIs allow game developers to test the waters with their existing games and skip much of the web3 implementation work. Stardust’s Core API product focuses on managing players and tokens with compatibility for three major chains (at least to start): Polygon, Immutable, and Solana. And within player management lives a custodial wallet service named Stardust Vault.

Even though the company has a much broader vision than just being a wallet solution provider, Stardust Vault is very interesting because its vision is to completely obfuscate the blockchain layer of blockchain gaming wallets for both game developers and players. In other words, games integrating Stardust Vault allow the blockchain wallet to live in the background fully and seamlessly integrate into the game’s narrative. Details remain scant, but Stardust is integrating with well-known L2s and game developers in the space, which signals big things for this wallet solution and the broader company. That said, it is still early days for Stardust Vault, and much needs to be proven before it can be considered the wallet solution experience for the masses.

Although both Horizon and Stardust might have originally taken a slow and steady approach by keeping their solutions in beta for a long time, both now show extremely high levels of polish. A frequent hurdle cited by web3 developers, especially on mobile, is the difficulty in onboarding new wallet users. While onboarding into new wallets might be greatly accelerated with the imminent rise of “Free-to-Own” (discussed later), both company wallet solutions have not only been developed to solve many of these early problems, but they are also battle-tested to a good extent. Although it’s a reach to think that every mobile developer is going to jump onto either Sequence or Stardust now immediately, we expect that their recent raises will help them make the choice for blockchain game developers much easier and thereby increasing the number of games using these wallet solutions, while having access to the necessary services and tools to smooth a major transition in mobile gaming.

The A-League Enables Distribution

When thinking about the mass adoption of blockchain gaming, it is obvious to think about how today’s key game distribution platforms will 100x the number of players blockchain games currently reach. Luckily, we can already see major platforms warming up to the idea or at least embracing the idea of taking their cuts.

First, Mythical Games made a big splash when Blankos Block Party offered the first NFT through Amazon’s Prime Gaming for free. And in September 2022, Blankos Block Party launched on the Epic Games Store! Further, Blankos Block Party also makes NFT onboarding easier by using custodial wallets, giving advanced users the option to use their wallets. The game also allows purchases using credit cards to avoid players needing to use any form of cryptocurrency. Given its easy onboarding, broad appeal, and exposure through the Epic Games Store, the game will help expand the blockchain gaming audience outside of its current niche.

While Blankos Block Party already has over 2 million registered accounts, getting exposure to the 180 million users of the Epic Games Store will undoubtedly stimulate the growth of the game’s audience. The bigger point though, is less about Blankos Block Party itself — this major release will likely be the beginning of a wave of many more games looking to the Epic Games Store as a viable launch and long-term distribution partner. This is especially important since Steam is still relatively unfriendly towards NFTs, while other alternatives like Mavis Hub have struggled to diversify beyond their own games. That said, it is still very early, and we should expect increased competition down the road.

Second, there has been a lot of ambiguity around selling NFTs in apps on the iOS platform. People have been able to purchase digital goods for a long time, but those goods could never truly leave the app to exist and be tradable elsewhere. According to the recently updated Apple App Store guidelines:

Revised 3.1.1: “If you want to unlock features or functionality within your app, (by way of example: subscriptions, in-game currencies, game levels, access to premium content, or unlocking a full version), you must use in-app purchase. Apps may not use their own mechanisms to unlock content or functionality, such as license keys, augmented reality markers, QR codes, cryptocurrencies and cryptocurrency wallets, etc. Apps and their metadata may not include buttons, external links, or other calls to action that direct customers to purchasing mechanisms other than in-app purchase, except as set forth in 3.1.3(a).”

Added to 3.1.1: “Apps may use in-app purchase to sell and sell services related to non-fungible tokens (NFTs), such as minting, listing, and transferring. Apps may allow users to view their own NFTs, provided that NFT ownership does not unlock features or functionality within the app. Apps may allow users to browse NFT collections owned by others, provided that the apps may not include buttons, external links, or other calls to action that direct customers to purchasing mechanisms other than in-app purchase.”

A couple of important callouts here:

- Apple now allows game developers to sell NFTs in apps through the in-app purchasing system using fiat (not cryptocurrencies) and thus pay a 30% fee to Apple. As the system follows the normal rules for in-app purchases (IAPs), the fee is only 15% for apps selling under $1M yearly. But that’s little consolidation for developers looking to web3 as a potential source of growth and a technology that idealistically evades oligopolistic middlemen.

- Ownership of the NFTs cannot unlock in-game features or functionality, which can be seen as a pretty major shot in the knee for a key value proposition of NFTs in the first place. Though it is interesting to note that today’s non-NFT virtual in-game items, when purchased as through IAP, do unlock in-game features and functionality, and it is clear that Apple wants to treat all in-app NFTs in the same way and ensure all NFT-related economic activity is conducted within their ecosystem. The additional clause added to 3.1.1 basically disallows folks from purchasing the NFT outside the Apple ecosystem and then use it in the game for any kind of in-game benefits.

While this increased clarity from a mega-platform should be a huge unlock and tailwind for game developers, it does lessen the ideological wish of no middlemen and end-to-end decentralization. Further, it directly attacks NFT ownership and tries to classify NFTs as just another virtual in-game item, which does reduce the utility of in-game NFT ownership altogether.

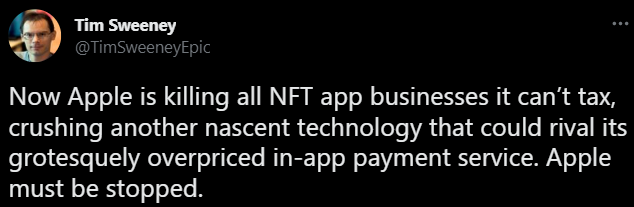

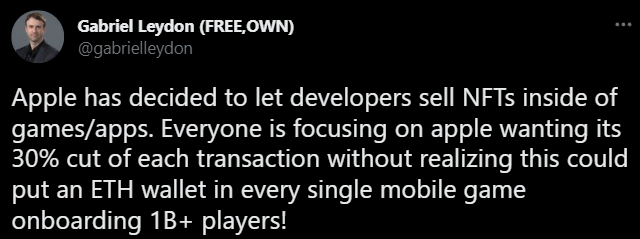

When The Information reported about Apple’s acknowledgement of NFTs, initial responses toward Apple’s news were fairly mixed, with Tim Sweeney of Epic Games (fresh off a long legal battle with Apple over App Store fees) coming out swinging in a tweet stating:

Others are taking the opposite approach and embracing the news, like Gabriel Leydon of Limit Break who is jokingly happy to give 30% of nothing since his company gives NFTs away for free while pioneering the “Free-to-Own” model. Leydon instead was very bullish on Apple explicitly allowing NFTs and providing much-needed clarity; he tweeted that:

With the business model for web3 gaming still evolving and many F2P mobile developers looking to move into the space, we do expect many developers willing to take direct revenue instead of crypto or tokens even at a 30% “loss.” It still seems sensible for the developers minting or selling NFTs directly to players to consider this move a positive. Still, any player-to-player transactions make little sense to happen in-app now – unless Apple also decides to extend its allowance of third-party payment providers for NFT transactions too. Developers may also allow items purchased in-app to be minted into NFTs at some point after the initial purchase, thereby reducing the number of on-chain transactions and gas fees. Furthermore, this rule only applies to buying. What about selling, trading, marketplaces, airdrops, and all the other unique things that NFTs can do? There's still much left to be addressed.

Further, developers will need to consider how they will make up for the reduced NFT utility when ownership cannot unlock and expose owners to new in-game content. That said, game developers have a solid track record of finding unique ways to work within Apple’s guidelines and deliver value to players. And Apple is also known to have changed their guidelines to service what’s best for both the customer and the developer.

Financial motivations aside, aspects of this counter to much of the decentralized ethos that blockchain advocates are excited about. It also exposes the real power dynamics at play (unsurprisingly, the platform with all the users gets to set terms in its favor). We expect a continued mixed reception of adopters and haters, a similar policy on Google’s side, and ongoing tweaks to the specific rules over time (perhaps some even due to new regulations). There is still some way to go here.

But regardless, these moves by Epic Games and Apple will significantly increase the presence of NFTs and web3 in mobile gaming, and mass distribution of blockchain gaming is very much on the horizon of mass adoption.

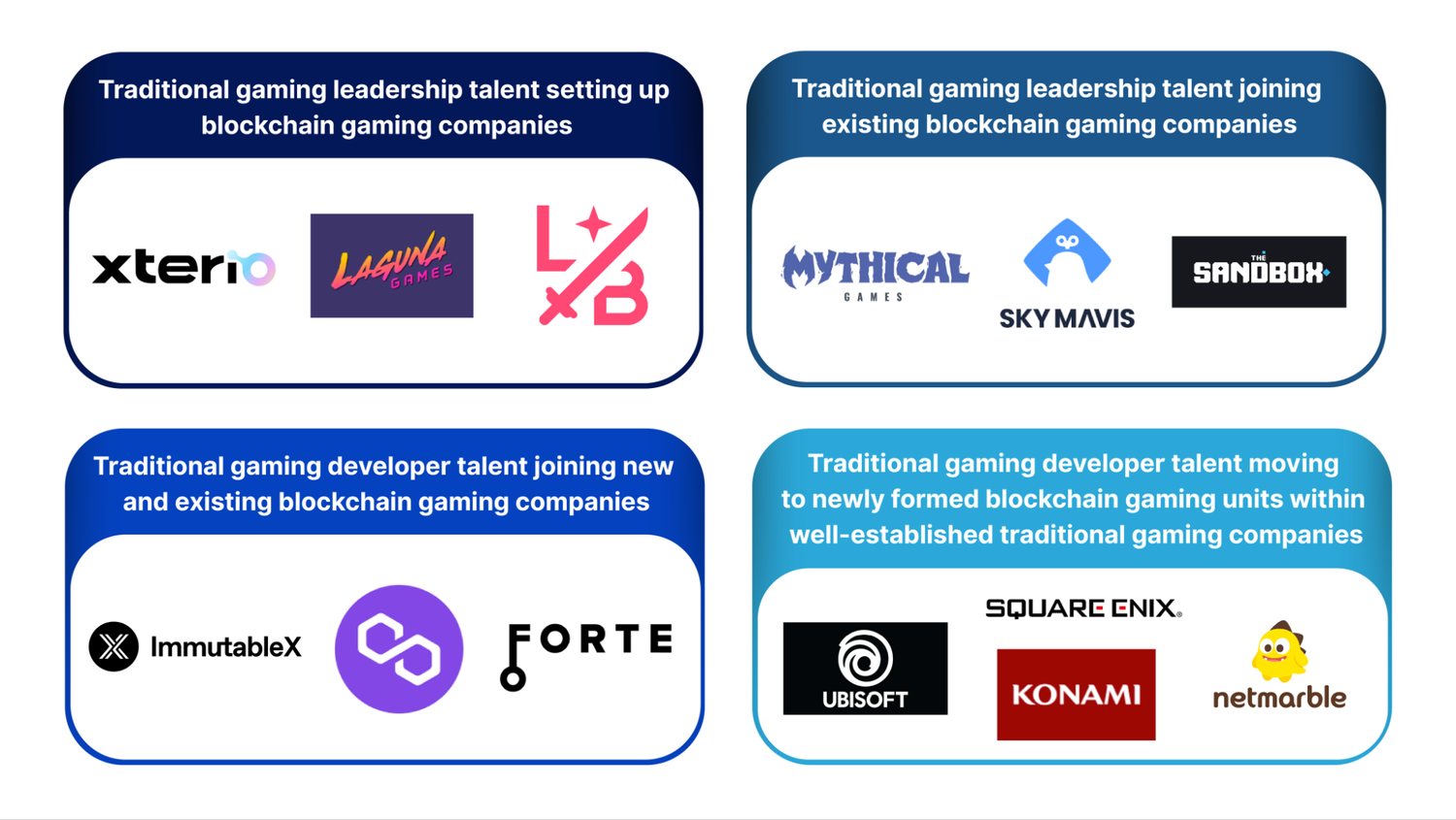

The Talent Migration has Begun

One of the biggest pet peeves of the traditional gaming industry has been that industry insiders are not building blockchain gaming companies and blockchain games. While this is not necessarily bad (fresh perspectives are always appreciated), it is also no longer true. The talent migration from traditional gaming (PC, Console and F2P) to blockchain gaming is now in effect. This transformation is playing out in four distinct ways:

- Traditional gaming leadership talent setting up blockchain gaming companies (Xterio, Laguna Games, Limit Break etc.)

- Traditional gaming leadership talent joining leadership positions in existing blockchain gaming companies (Mythical Games, Sky Mavis, The Sandbox etc.)

- Traditional gaming developer talent joining both new and existing blockchain gaming companies (Immutable, Polygon, Forte etc.)

- Traditional gaming developer talent moving to newly formed blockchain gaming units within well-established traditional gaming companies (Ubisoft, Square Enix, Konami, Netmarble etc.)

And here are how the hiring numbers are currently playing out for key companies in the space:

While this migration will be slow and steady, its impact on the blockchain gaming space will almost surely result in games that are not only more fun to play, but also built on the back of traditional gaming best practices. This should also accelerate the quest toward more widespread economic sustainability in the open economies of blockchain games.

From P2E to F2O

As previously discussed, the fall of the P2E business model is upon us. Even though Axie Infinity is the poster child of the same, the bigger picture that companies like Sky Mavis and projects like Loot, Gods Unchained, and Dark Forest have showcased to the rest of the gaming industry is that there is a kernel of value in blockchain gaming that can be built further upon. And that’s exactly what today’s teams are building towards.

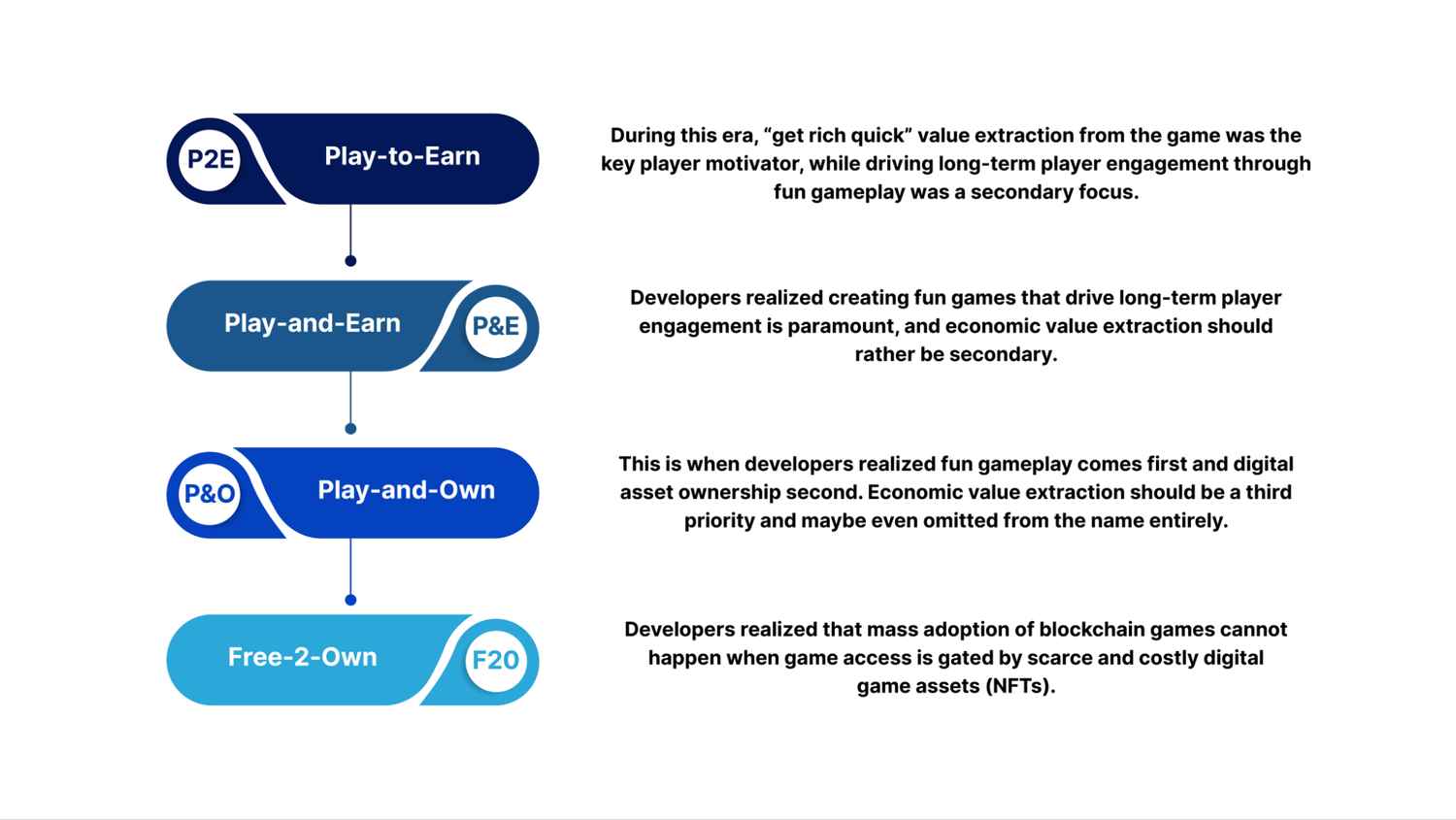

The evolution in product thinking is seen in how business model terminology has evolved since 2021:

- P2E (Play-to-Earn): During this era, “get rich quick” value extraction (in the form of earnings) from the game was the key player motivator while driving long-term player engagement through fun gameplay was a secondary focus. Economically unsustainable design brought these types of games down because people tried to extract more value than they created, and at scale, that led to financial speculation-driven bubbles.

- P&E (Play-and-Earn): This was when developers realized creating fun games that drive long-term player engagement is paramount, and economic value extraction should rather be secondary. Unfortunately, the name change didn’t result in quick design and economic pivots of existing products but achieved a key mindset shift for developers building towards the future of blockchain gaming. That said, P&E was a doomed to fail half-step. What it got right is that playing to earn was wrong, but it didn't quite make the full step that earning itself still shouldn't be a primary motivator on par with playing/fun.

- P&O (Play-and-Own): As the P&E era was short-lived, it was immediately followed by the P&O era when developers realized that economic value extraction should be the third priority and maybe even omitted from the name entirely. It should rather be preceded by fun gameplay first and digital asset ownership second. In other words, the mindset now was “get the first two right, and the third will follow” because provable digital asset ownership is a key and unique value unlock that blockchain brings to games. This was another mindset shift milestone.

- F2O (Free-2-Own): Again, the P&O era was a short-lived one, and we are now amid a new buzzword – F2O – which is spearheaded by none other than Gabriel Leydon’s new company, Limit Break. Developers have realized that mass adoption of blockchain games cannot happen when game access is gated by scarce and costly digital game assets (NFTs). So why not offer NFTs for free to start, upsell to whales later, and then pocket royalties on trading? While F2O is still in the making, and we’d be hesitant to call it an era of its own just yet, the similarities to traditional gaming are strong in that there’ll likely be many different styles/genres, with F2O being one (like F2P). However, other ways can still succeed when done right.

So what exactly is F2O? In a post about the subject, Alok Vasudev of Standard Crypto writes:

“F2O is a natural evolution in a decades-long power shift from the game developer to the player. The first video games were arcade games where players had to pay every time they played the game. Next came console games where players had to pay a high one-time price (e.g. $60) for a game that they could then play unlimited times. Early mobile games, which followed, continued the console model but with a much lower one-time price (e.g. $1). Mobile games evolved into free-to-play (F2P) where players no longer needed to pay at all to play the game and game devs needed to earn the right over time to get paid – typically by selling in-game assets.

F2O takes this one step further. Game devs give away a portion of the assets they'd otherwise have sold to players. Players co-own the game economy alongside the game devs. F2P is “freemium”; F2O is “less than free”. F2O is still a work in progress but its core mechanism involves offering players of a game (or future game) the opportunity to mint – for free – digital assets of value within a game economy. The assets are built as NFTs so players have true ownership of the digital assets they acquire for free. The NFTs have a creator royalty mechanism where game devs make money as a percentage of the game economy’s “GDP”.”

It's a solid articulation in which the illusion of F2P is turned on its head. The killer feature of F2O is the simple fact that it dramatically lowers barriers to entry by offering NFTs for free and not gating game access with sometimes absorbently high NFT (of multiple NFTs) purchase prices. This could be an important catalyst for accelerating the mass market adoption of blockchain gaming.

So how does Limit Break fit into all of this? We first learned of MZ co-founder and former CEO Gabriel Leydon’s new initiative with Limit Break during his interview on Invest Like The Best almost a year ago. The company has been in stealth mode for quite a while until they recently announced a $200M raise at a reported $1.8B valuation! The latest fundraising announcement included details about Leydon’s “new” take on web3 gaming — Free-to-Own.

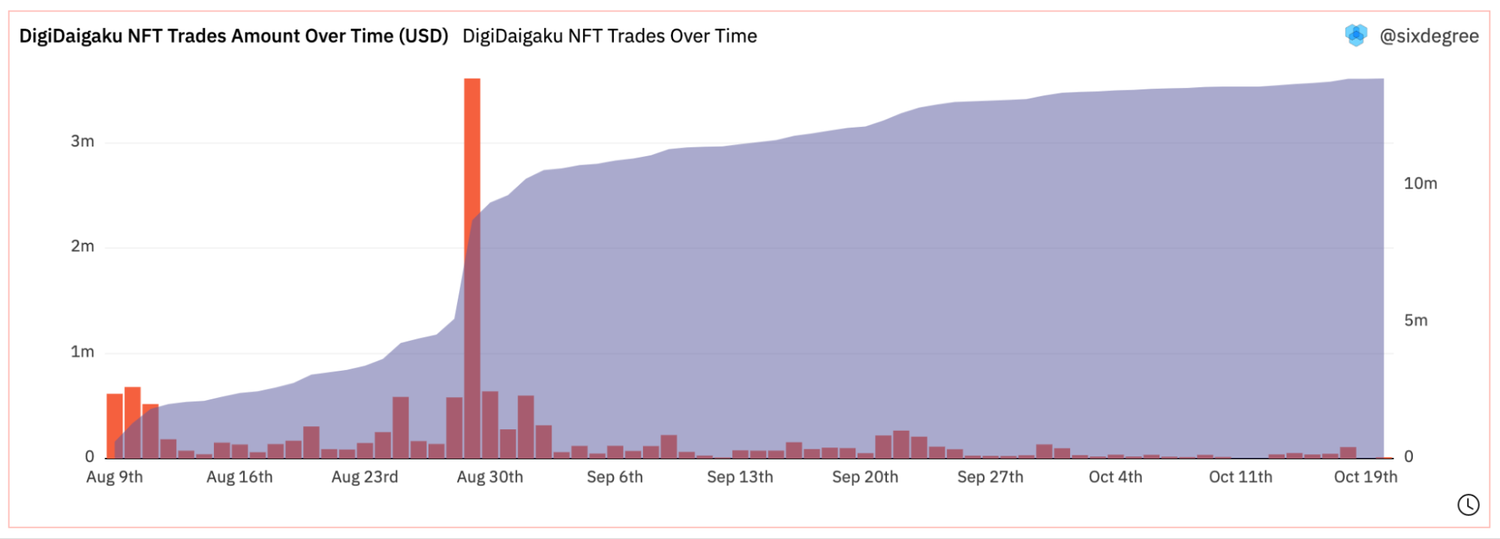

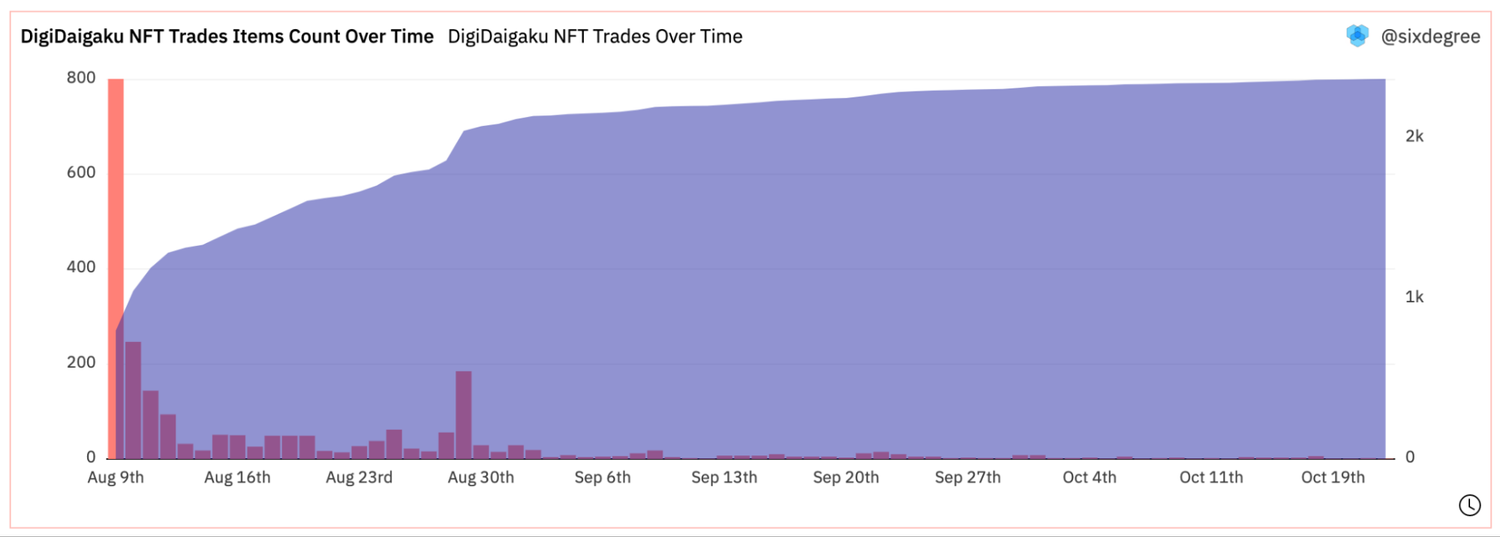

This model is counter to the current NFT pre-sale culture. Much like with the previous pivot from premium games to F2P on mobile, F2O evolves the idea of free downloads into free NFTs, fully embracing the concept of democratizing digital ownership at scale. Limit Break kicked this off with the stealth and free mint release of its DigiDaigaku NFTs, with 2,022 available, which sold out very quickly and have already done over $13M in secondary market transactions. Suppose you’re still wondering what exactly the innovation here is – with Limit Break, by giving away rather than selling the initial batch of NFTs, Leydon is not only marketing the project successfully but also creating a core advocacy community of players who are much less likely to be disappointed by financial returns as they didn’t pay anything to join.

Although demand has since died down due to no specific utility revealed, the OpenSea floor currently price sits at 11.5 ETH (as of October 21st), or ~$14.8K.

These won’t be the only NFTs from the new brand, especially given the small quantity, so initial demand for future NFTs should be even higher. And just because some NFTs are free to mint doesn’t mean that all NFTs will always be free. Limit Break does intend to reserve some NFT assets to sell later as part of its business model but only after they have good financial traction on peer-to-peer marketplaces. It’s hard to say if this is a sound business tactic, as the price Limit Break sells them for can’t be too high or it will look greedy, or too low and it will look like they are undermining the existing players. There are other revenue sources too, such as market transaction fees, and we imagine more yet to be revealed. While a lot remains unclear at the moment, especially what kind of game Limit Break is building and how the economy of that game is designed for long-term sustainability, Leydon has made his intentions to be the #1 web3 game very clear. These steps are simply one piece of a much larger unannounced project.

Finally, Leydon is putting his money where his mouth is by planning a $6.5M Super Bowl ad for his game DigiDaigaku! The 30-second ad slot will enable Limit Break to show off DigiDaigaku in a commercial at Super Bowl LVII in February 2023 in support of the game’s community. It’s a first for a blockchain gaming community to have a Super Bowl ad that could be viewed by more than 50 million live viewers and tens of millions more online. And who knows - maybe there are free NFTs to pick up if you’re watching!

Will F2O be the last business model buzzword we see? While that’s hard to say, there are a few important points to keep in mind about how Limit Break specifically views the upside of this model:

- It’s easier to onboard someone to an NFT and then to crypto rather than the other way around.

- One can give away all the free NFTs they want on mobile platforms without paying any fee because 30% of $0 on mobile platforms is $0.

- The games that will truly see mass market success are those that lean into digital asset abundance more so than extreme scarcity. That said, there will likely be a place for digital assets scarcity given its proven economic upside, but not all digital assets need to be or should be scarce.

- As exemplified by Limit Break, F2O teams do have the opportunity to raise large sums of money to pursue massive marketing and user acquisition tactics (like the Super Bowl ad). Take this with a pinch of salt though because Leydon has proven experience running Super Bowl ad campaigns (twice!) during his time at Machine Zone.

All that said, while F2O is a significant product thinking evolution, it isn’t the only one of its kind currently occurring in the market. Here are a few companies and trends that intrigue us – all of which you can learn more about in Naavik Pro.

Playmint and On-chain Gaming: Heavily inspired by on-chain games like Loot and Dark Forest, Playmint is on a mission to build category-defining web3 games, not web 2.5. Its first title, The Crypt, is a loot-based dungeon game that exists entirely on the blockchain and enables anyone to build on top of it. As the world’s first player vs environment co-op on-chain game, players can build their own clients, bots, and even their own games using the primitives that Playmint has developed. Playmint is taking key learnings from building chapters of The Crypt to build its second title, an on-chain trading game full of politics, subterfuge, and economic opportunity. It will be interesting to see how companies like Playmint building on-chain games fully embrace the underlying blockchain technology to drive product design decisions.

First Light Games and F2P Blockchain Gaming: First Light Games is one of many companies exploring this strategy with their game Blast Royale. This will be a free-to-play game in which players can play on any available platform for free. This means that players will not have to make upfront payments (in the form of NFTs, for example) in the game to play and will be allowed to play using in-game items that aren’t NFTs. And once players are mentally ready to spend money, they can buy into the NFT/Token economy, which is very similar to how F2P games monetize small portions of their large audiences. Furthermore, these studios are applying many F2P design best practices to drive engagement in their products. The convergence of the F2P and P2E/P&E business models was almost inevitable, and it will be interesting to see how it evolves going forward.

Xterio and Evolving Tokenonimics Models: Even though Xterio is a tool and platform provider for blockchain game developers, it wants to publish first-party games too. The difference, though, is that it intends to have the economies of its games all interact with one game ecosystem token called XTER. While the deeper details are available on Naavik Pro, game ecosystem tokenonomics is something that both Animoca Brands (with the REVV token) and Joyride Games (with the RALLY token) are exploring across their gaming ecosystems. Further, companies like Rooniverse are experimenting with a one-token economy, while companies like Mythical Games are questioning the existence of tokens altogether. This shows how quickly some of the economy design baselines set by the first era of blockchain games (like Axie Infinity’s two-token economy) are being challenged and improved upon in a quest for tokenomics best practices across the space.

Joyride Games and Genre Expansion: After releasing one of the quicker DappRadar chart-toppers in recent months (Solitaire Blitz), Joyride Games hit another success (at least by blockchain game standards so far) with the release of Trickshot Blitz on August 15th. Both games are quite casual versus the typical mid-core focus that blockchain games have generally had. It shows how game developers are expanding their thinking outside the “obviously-fitting” genres to capture new genre blue oceans in blockchain gaming.

Laguna Games and Audience Expansion: As we already know, the number of blockchain gamers today is quite small versus the total global player base, especially mobile. Further, user acquisition tactics in blockchain gaming are nowhere near as formalized or systematized as in mobile F2P. Therefore, studios are hungry to find new ways to expand their game audiences. Laguna Games has announced plans to release four new hypercasual mobile games (all quite different from each other) based on the Crypto Unicorns IP during Q4 this year. While we do question the shotgun approach and potential audience mismatch of this strategy (hypercasual gamers are a huge audience on mobile but also very fickle in terms of retention and monetization), the broader takeaway is how studios are experimenting with new methods to broaden their game’s top of the funnel massively.

Square Enix and Asian Blockchain Gaming: Japanese game developer Square Enix has been vocal about its desire to move toward a blockchain- and NFT-oriented future despite backlash from fans on social media. The company recently continued its path with an announced initiative with blockchain Oasys. Oasys is part of a growing trend in Asian countries, such as South Korea and Japan, of creating blockchains with the support of regional game developers, thereby fueling the local blockchain gaming ecosystem. South Korea, for example, has the Klaytn blockchain, which is also looking to support general metaverse projects. On the game developer side, Bandai Namco intends to build metaverse and NFT projects for Dragon Ball and Gundam. SEGA has publicly talked about its future Super Game “framework,” intending to be a multi-game project using cloud and NFT technology. Com2Us is building out its blockchain gaming platform, C2X, that will eventually host blockchain games using the Summoners War IP. The combined IP power of just four three companies alone could be a huge unlock for great blockchain gaming content coming from the East, and they all seem intent on leveraging that IP.

Shrapnel and UGC: Shrapnel is important because it represents a high-quality AAA game in the burgeoning genre of extraction shooters and has a very well-thought-out player creation economy design. User-Generated Content (UGC) has become a hot topic in relation to web3 because of the potential for earnings through tokens and ownership through NFTs. Rather than being part of a bolted-on system or mod creation tool, UGC is deeply ingrained in Shrapnel’s gameplay, economy and meta-gameplay loops. Realistically, it’s fair to say that the gameplay integration is more akin to crafting than full-fledged UGC, with the UGC-like parts focused on vanity gear and map creation. Regardless, the future of UGC in web3 is one trend to keep an eye on, especially with games like Shrapnel, The Sandbox, Decentraland, Axie Infinity, and more all going after that opportunity.

Delysium and AI in Blockchain Games: Delysium is a pretty standard battle royale game, but one of its big differentiators is a major focus on AI participation through its “AI MetaBeings” — which Deterrance enables, the first AI tech layer that powers “intelligent NFTs”. These NPCs can act as teammates/companions, learn from you, and even participate in the economy. While you can find more details on Naavik Pro, we shouldn’t miss the forest for the trees, as Delysium is just scraping the surface of integrating AI into blockchain games. A broader revolution is brewing across the games industry in which AI touches many more aspects of the game, the game development process, and its audience. The other big differentiator is that Delysium will let certain users create their modified servers of the game (including unique game economies), unlocking an interesting and competitive UGC layer, and we’re curious to see how that goes.

Between P2E, P&E, P&O, F2O and all the above-mentioned product trends, the industry will hopefully start converging on an ideal web model for web3. In reality, the ongoing evolution of these ideas is unstoppable! What’s more definite is that best practices that define the future of blockchain gaming are very much in the making. There is some truth to the cliche “these early years of blockchain gaming feel very similar to the early years of F2P”.

Regulation is Coming, Fast

Regulation has been nothing less than a sleeping dragon for the blockchain gaming space. While 2020 and 2021 were truly the wild west years in terms of what developers and players could get away with, these years were also fraught with major value destruction hacks and scandals that just cannot be turned a blind eye to. Regulation was always coming, but regulatory bodies clearly started to notice in 2022. And this is not just limited to blockchain gaming but the broader crypto space too.