Welcome to Master the Meta, the #1 newsletter analysing the business strategy of the gaming industry.

This company deep dive is a collaboration between Aaron Bush and Abhimanyu Kumar from Master the Meta, a newsletter analysing the business strategy of the gaming industry, and Joakim Achren from Elite Game Developers, an online resource that helps gaming entrepreneurs reach success in the industry.

Hi everyone,

Stillfront Group is an emerging games business that both industry insiders and curious outsiders should prioritize understanding. Even though the company is making a larger name for itself — especially in 2020, which has turned into a breakout year — it remains, in our eyes, underrated and under-followed. It was (and maybe still is) a dark horse of the games industry. Tripling its market cap year-to-date certainly helps, but most don’t understand how Stillfront’s unique acquisition strategy, group operations culture, and capital allocation skill bring consistency and scalability to an otherwise lumpy, hits-driven industry. In other words, Stillfront’s success is the result of a well engineered strategy designed to predictably grow shareholder value in a highly unpredictable market. The long-term view of Stillfront’s stock price speaks for itself!

Naturally, we had to take a look under the hood to understand how Stillfront is achieving such striking outperformance. This deep dive covers various aspects of Stillfront’s history, current business strategy, and our take on the company’s future. It also builds on top of our interview with Stillfront’s CEO and Co-founder, Jörgen Larsson, which you can find here. Let’s dig in!

Jörgen’s Story

The first step to understanding Stillfront is to understand the man behind the business - CEO and Co-founder, Jörgen Larrson.

Jörgen thoroughly describes his entrepreneurial journey up until founding Stillfront in the podcast linked above, but there are four points about his journey that distinctly stand out to us:

- First, he has loved playing games since his childhood (Chess being his favorite), considers gaming to be a key human need, and believes there’s still much to be explored in online and internet-related gaming.

- Second, he realized and embraced the much bigger business potential of free-to-play (F2P) games versus traditional off-the-shelf titles.

- Third, he’s passionate about building businesses, actually founded four companies in his career, and learnt, improved on, and implemented those insights into every successive venture.

- Fourth, he understood the unique business model benefits of managing a portfolio of proven long lifecycle games versus going down the well trodden path of “just building a great game” that usually has an unfavorable risk/reward ratio.

In short, Jörgen comes across as not only a highly self-reflective and experienced entrepreneur, but he also has a sharp business mind in both a qualitative and quantitative sense. His approach to tackling the F2P market is very different compared to many other entrepreneurs who want to build massive gaming businesses, and we think that distinction is ultimately wise. Stillfront is obviously larger than one man — and our time together was relatively brief — but we suspect the four points above are key factors that led to what Stillfront Group ultimately became.

Listen to his story here:

Stillfront’s Journey to Present Day

Jörgen himself describes Stillfront’s journey in three phases, which we paraphrase as:

- 2010-2015: Before Stillfront went public, many internal processes that lay the foundation for future business growth still need to be improved on. The team used the early years to iterate on multiple elements of the business — strategy, decentralized culture, etc.

- 2015-2019: Recent years have focused on M&A execution and becoming the best home for great industry talent. Elevating the business by attracting and retaining successful studio teams was front and center.

- 2019 to now: Stillfront is currently focused on scaling, plus better understanding and leaning into its competitive advantages, which should take the business to new heights and ultimately closer to becoming a F2P powerhouse.

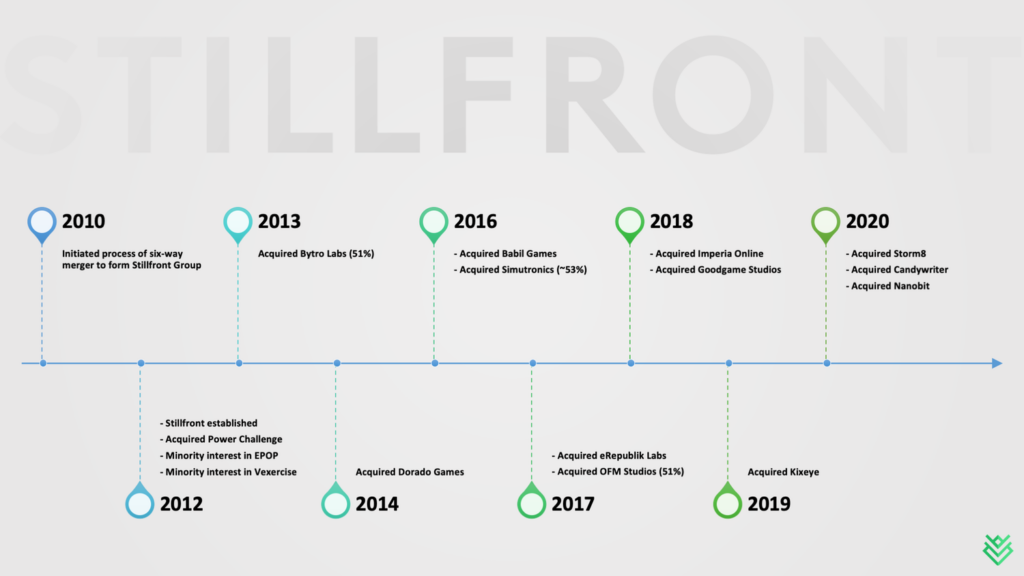

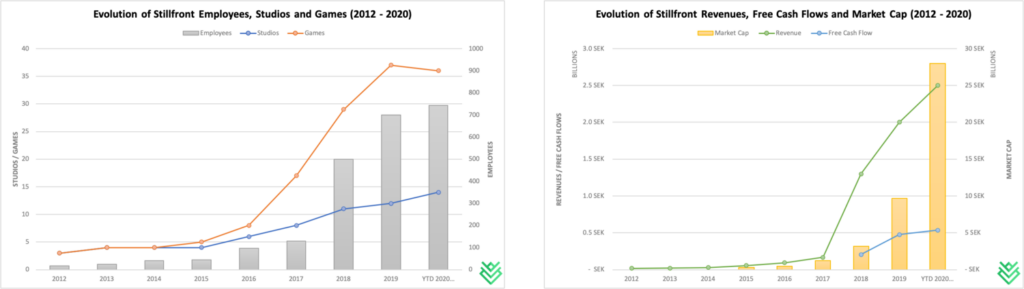

With that context, let’s back up for a moment and start at the beginning. Stillfront was founded in 2010, but truly came together in 2012 when six companies — Stillfront, Coldwood Interactive, OnGolf, Gamerock, VOIPlay, and Verrano — merged. That’s an unusual beginning on the face of it, but the purpose was clear: to create significant value by forming a roll-up entity for consistently profitable gaming studios that ideally have further room to grow. And over the last decade, as depicted in the timeline below, Stillfront has demonstrably executed on its mission:

The timeline offers three observations. First, Stillfront historically acquired and integrated approximately one studio per year (plus other partial interests), but the pace and size of those deals have definitely picked up more recently. As we write, 2020 is running at a rate of 1 studio per quarter versus 1-2 per year in previous years. Further, 2020’s deals are considerably bigger than they were in previous years. For example, Storm8 was acquired for up to $400 million, which is larger than Stillfront’s entire market cap only a few years ago! Stillfront now includes 15 studios that are spread around the globe both in terms of offices and sales. It should be noted that Stillfront is in the business of enabling these studios to build great games, not acqui-hiring these teams to make specific games as dictated by a corporate overlord. This strategy of acquiring, integrating, developing, and growing game studios in a highly decentralized fashion has propelled the business to a $4.4 billion market cap over the last 5 years. And there’s further expansion ahead.

Second, as Stillfront grew, its bench of leadership talent increased as well. Acquiring other studios led to many studio leaders taking on larger and more impactful roles at the parent company level:

- Alexis Bonte (Stillfront COO) joined when eRepublik Labs was acquired.

- Phillip Knust (Stillfront CPO) joined when Goodgame Studios was acquired.

- Clayton Stark (Stillfront CTO) joined when Kixeye was acquired.

And, of course, as Stillfront grew in size and complexity it also attracted leaders like Andreas Uddma (the CFO) and Marina Andersson (Head of M&A), who both joined in 2019. One benefit of ongoing growth and acquisitions is that the company should continue to attract proven leaders that ideally face opportunities to scale their impacts. Another benefit is how each of the group-level executives have very focused areas of expertise, such as Phillip Knust who was the creative founder of Goodgame Studios’ two biggest gaming brands - EMPIRE and BIG. Building gaming brands such as these is no easy feat. It only makes sense that Stillfront utilizes these specific areas of expertise and finds ways to scale their lessons across the entire enterprise so all studios can benefit. Finally, integrating key leaders of the acquired units into Stillfront’s leadership team builds cultural alignment — ensuring studio-specific cultures are maintained while at the same time adapting to be part of a bigger family.

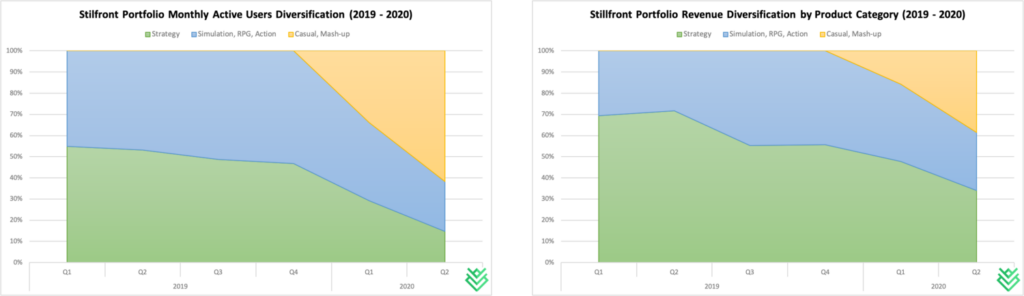

Third, there is a clear evolution in the F2P game genres that Stillfront is expanding into through its acquired units. The company’s original focus was primarily on browser based F2P strategy games, which naturally lean toward higher retention within relatively niche audiences - one definition of long lifecycle games. However, after many years and numerous acquisitions Stillfront’s studio count, genre mix, platform exposure, and geographic diversity increasingly widened. As of Q2 2020, 75% of bookings came from mobile, an area Stillfront had no exposure to in its early days. The genre focus has expanded beyond strategy to now three core areas: Casual/Mash-up (38% of bookings), Strategy (34% of bookings), and Simulation/RPG/Action (28% of bookings). And geographic revenues evolved to be mostly split between Europe and North America but with emerging growth in other regions. Of course, that mix will continue to evolve as different games succeed, new studios are tucked in, and as Stillfront’ evolves its overall strategy.

These observations are reflective of three key strategies that Stillfront uses to scale the business and create significant value:

- Centralizing capital allocation decisions, primarily to pursue financially flexible M&A

- Embracing a highly selective acquisition process, while diversifying to reduce portfolio risk

- Keeping studio operations decentralized, while still driving synergies throughout the group

These strategies result in an environment that breeds autonomy, shared upside, minimized risk, a focus on high margin, recurring revenues, and a constant eye for new deals. This approach has scaled remarkably well in other industries (thinking about Constellation Software, Transdigm, etc.), but it’s still relatively unique in gaming, which is traditionally viewed as a hits-driven business. And when this strategy was put forward 10 years ago by Jörgen Larsson — at a time when mobile gaming was still beginning to ramp up — it was even more of an under-the-radar opportunity.

Now let’s dive deeper into each separate strategy…

A Deeper Look into Stillfront’s Strategy

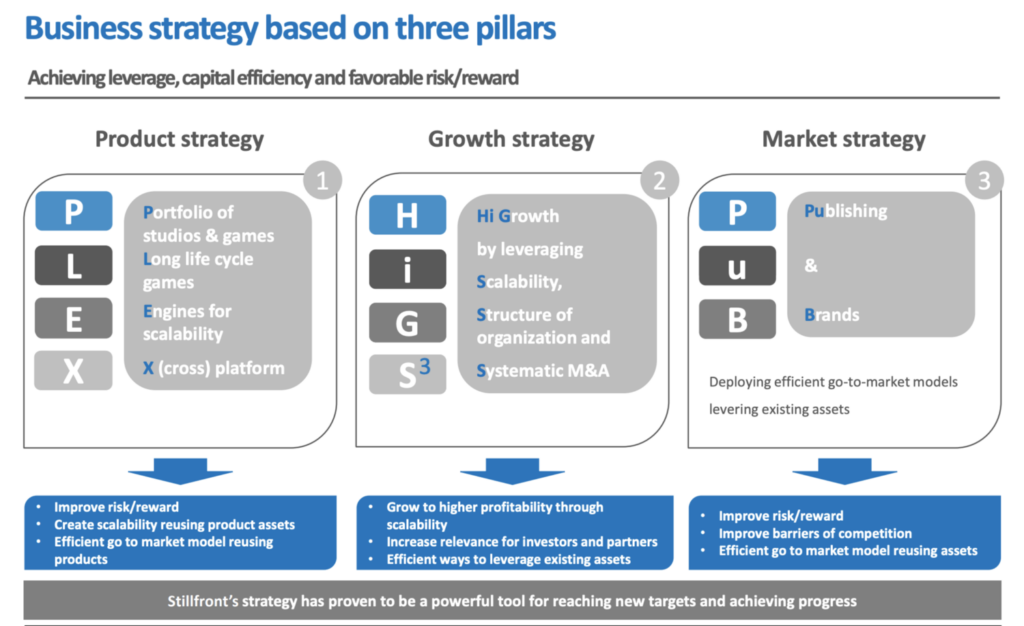

Stillfront’s goal is to consistently and predictably grow value for all relevant stakeholders within a traditionally unpredictable and hits-driven industry. In Stillfront’s eyes, it achieves this through a three-pillared approach called “PLEX + HiGS3 + PuB” (try saying that five times quickly!), which is defined in the image below. In practice, Stillfront brings this to life by executing on the three key strategies mentioned above.

Strategy #1: Centralizing capital allocation decisions, primarily to pursue financially flexible M&A

This strategy is the keystone to how Stillfront has grown so much so quickly. All of the studios run their own decentralized businesses, and the leftover cash — plus whatever money the company raises in other ways — heads to HQ where Jörgen and team decide how to best reinvest it. Stillfront’s financing approach has proven to be flexible (various mixtures of cash on hand, debt, and stock), and the company is highly selective in what they actually buy (and at what price).

It’s worth noting a couple financial realities. First is simply how profitable Stillfront is. As a result of selective acquisitions that focus on engaging and profitable studios, Stillfront consistently generates 30%+ EBIT margins, and the majority of those operating profits translate into free cash flow. This not only reduces risk and traditional lumpiness — especially if those profits come from increasingly diverse sources — but it provides the cash that is effectively reinvested back into acquisitions.

Second, even though cash flows are starting to add up, it hasn’t been enough to strike large deals with. So the company has resorted to leveraging debt and equity. Stillfront now has net debt of SEK 665M (~$74M), which can easily be covered with future cash flows. Leverage ratios are always important to watch, but management has set guide rails — a target maximum leverage ratio of 1.5x — to ensure risk is mitigated. Furthermore, selling equity is dilutive, but Stillfront’s use of shares has generally been positive. After all, selling shares at 40x EBITDA to buy companies at a fraction of those multiples is a worthwhile exchange, especially when high margin revenues are steady and the studio teams also become incentivized to help Stillfront grow to new highs. Of course, if Stillfront sells more equity (which is likely), the balance sheet could shift into a net-cash position, but since that financial ammo would be used for acquisitions it likely wouldn’t stay that way for long. Also, even though diluted share count grew ~22% over the past two years to help pay for deals, existing shareholders received far more upside in return.

In other words, Stillfront’s financial approach is aggressive in terms of action but fairly conservative in terms of what debt it’s willing to take on and what it’s willing to pay for deals. And the company’s use of various financial levers ensures it’s always thinking about what makes the most sense to use in any given situation. Many people will say Stillfront’s share appreciation is primarily a result of multiple expansion, which is partially true, but it’s important to understand why multiples expanded so much in the first place. As you can see in the table below, the company’s capital allocation approach has resulted in pretty remarkable growth (which, paired with Stillfront’s relative financial conservatism, is even more noteworthy):

Some of these factors are even more striking in chart form:

Keep in mind, it’s tough to pin down the company’s exact financials, because Stillfront continues to make moves! If we add in Nanobit (acquired in September), which contributes several more games (~19) + employees (~125), over SEK 600 million of estimated 2020 net revenue, and delivers ~20% EBIT margins, Stillfront’s trajectory looks even better.

Strategy #2: Embracing a highly selective acquisition process, while diversifying to reduce portfolio risk

We’ve established that M&A is core to Stillfront’s strategy, and, so far at least, leadership’s done a good job striking deals in ways that are rewarding for everyone. Obviously profits play a key role in picking acquisition targets, but observing Stillfront’s portfolio of acquired studios uncovers five other important commonalities:

- Studios with portfolios of long lifecycle games

- Studios who have the skills but not the resources to unlock their next stages of growth

- Studios with reusable game engines that can generate new titles and build genre focus

- Studios with exposure to different geographies

- Studios that diversify across genres, platforms, and other factors.

Studios with portfolios of long lifecycle games: By “games with long lifecycles,” we mean games with strong long-term retention, long-tail monetization profiles, and therefore very healthy long-term player lifetime values. One can immediately see how acquiring companies with such product portfolios immediately contributes to highly attractive profit margins and thereby increases business predictability for Stillfront.

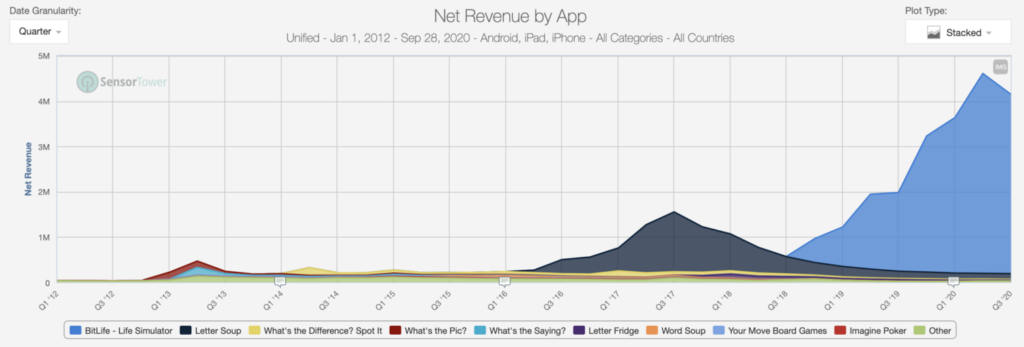

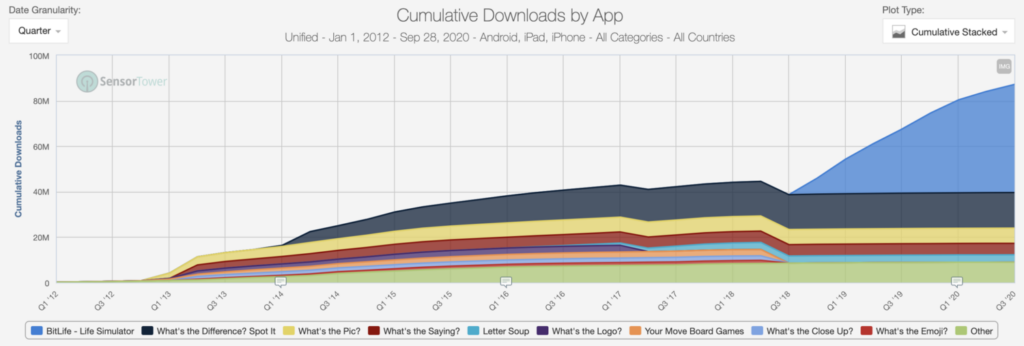

Almost each and every one of Stillfront’s acquisitions fits this criteria perfectly, which reiterates just how important recurring revenues are to the company’s leaders. The only studio that we weren’t able to instantly figure out was Candywriter, but with Sensor Tower’s help, the data tells us that there are two Candywriter games that could also fit this property. The first is the word game “Letter Soup”, which looks to be more of a medium lifecycle title. The second, and most surprising one, is a life simulator game “BitLife”, that is able to grow revenues on dropping downloads. Not only that, but it is an entirely new game concept that the market has not really seen before.

On top of all this, Candywriter boasts a very impressive 84M lifetime downloads number as of Q2 2020, which brings massive audience scale to Stillfront’s portfolio. In light of the upcoming IDFA apocalypse, this audience scale will definitely prove to be useful.

Lastly, it’s important to note that not all game genres can support long lifecycles, mainly because meta gameplay depth differs from genre to genre. And most genres with deep meta gameplay usually survive when niche or highly engaged audiences remain dedicated to the games for long periods of time (~3-5 years). Both points help explain Stillfront’s initial focus on the Strategy genre and its eventual expansion into Simulation, RPG, and finally Puzzle. The beauty of the Puzzle genre is that it’s one of the few genres that not only has broad audience appeal, but it can also support healthy long-term player lifetime values. Having said that, there are still more genres with similar metric profiles but not yet in Stillfront’s portfolio. That’s more opportunity for Stillfront!

Studios who have the skill, but not the resources to unlock their next stage of growth: This commonality is likely a key factor in deciding whom to target to acquire. Not only does it make the conversation to acquire easier, but also offers Stillfront the opportunity to strongly sell its value add to potential targets. Probably the best way to validate it is by looking at the mobile revenue trends of some of the recent acquisitions, until Stillfront came into the picture.

The picture above makes two points clear. First, the bigger acquisitions Stillfront made (Storm8 and Goodgame), were performed at a time when both the bigger studios reached or were about to reach some level of revenue stagnation across their entire portfolio. Second, the smaller acquisitions Stillfront made (Nanobit, Candywriter and Kixeye), were performed at a time when these smaller studios were likely hitting their peaks in terms of foreseeable growth potential. And again, Stillfront could be the one to unlock their next stage of growth. In either scenario, the target studios have either proven revenue scale or a proven team/skills or both, but Stillfront could be the one to elevate their businesses even further. Most definitely, the bigger the group gets and the more sophisticated its platform becomes, the easier it might become to sell this value to prospective acquisition targets.

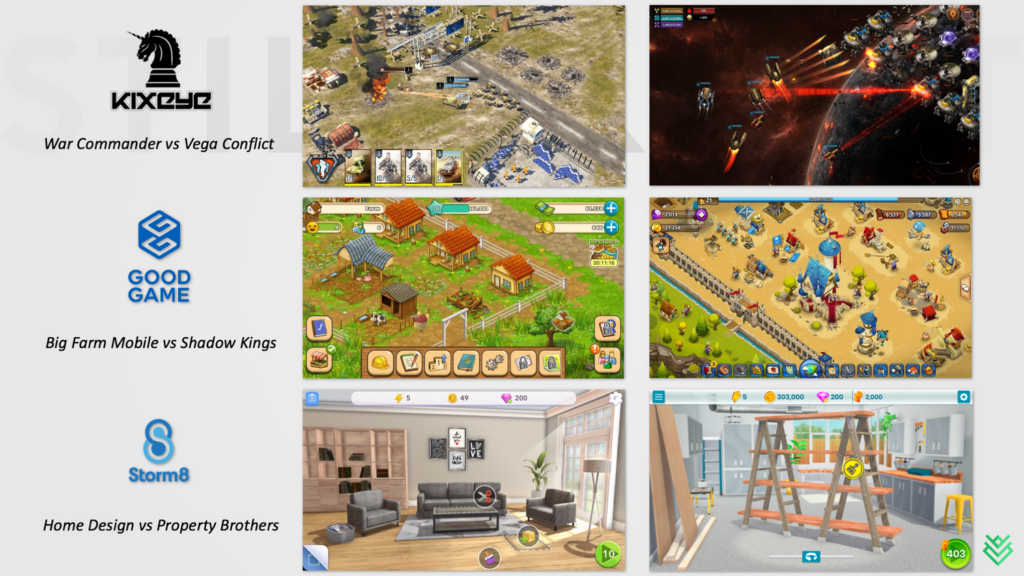

Studios with reusable game engines that can generate new titles and build genre focus: Many of Stillfront’s acquired studios seem to have game engines that can be reused to generate new titles in an almost templatized fashion, which makes the deals even more savvy. Note that when we say “game engine,” this could include both proprietary in-house game engines or studio-specific customizations built on top of existing game engines like Unity.

Not only does this point reduce game production timelines, but every consequent title ends up better than the previous one. This is because the game engine is ever-evolving, and learnings from previous titles can be plowed back into new titles, which automatically results in increased business value. This obviously ties back to studios building genre focus and slowly gaining genre mastery. While creating game sequels could be one way to generate new titles using this method, another approach could be to re-skin games with new themes, so as to cater to a wider variety of audiences and preferences. Check out below how this plays out across Kixeye’s, Goodgame’s, and Storm8’s products.

Studios with exposure to different geographies: There are two aspects to this facet of the acquisition strategy - personnel and revenues. In terms of personnel, having a global set of offices results in some strategic advantages that can be taken advantage of across the group. The most obvious one is easier access to a global talent pool, and Stillfront definitely has a global personnel footprint. Some regions have lower labor costs, as well, which is beneficial to profit margins.

More importantly (and revenue related), footholds in multiple regions provide Stillfront deeper, more intricate insights into many corners of the world. This understanding can be used to customize product launch strategies, find fitting design and monetization approaches, and organically localize game experiences — all of which strengthen players’ experiences. The end result is increased market penetration, boosted player engagement, and maximised business value per project.

As you can see in the image above, while Stillfront already has a strong presence in the USA, Europe, and Australia, more opportunity in key growth markets like China, LATAM, India, SEA, and Russia remains to be captured. Last quarter, only 19% of sales came from regions other than North America and Europe, which signals plenty of global runway. In general, it’s encouraging to see how Stillfront’s has worked towards creating a product portfolio in which the three product categories rake in significant revenues from different regions.

Studios that diversify across genres, platforms, teams, and other factors: Given how fast moving and ever-evolving the games industry is, consistently growing shareholder value necessitates proactively limiting downside, which requires diversification — across the number of games, the genres of games, the platforms, and also the teams. Keep in mind, Stillfront started off with a mixed bag of PC and console developers, then moved to F2P browser-based strategy games, and most recently it’s been acquiring mobile studios across game genres and countries. In other words, Stillfront currently has knowledge that touches PC, console, and mobile, games that span across multiple genres, and teams that are globally distributed.

This is not a new or unique strategy by any means (think about Applovin or today’s Zynga for reference), but it is important and Stillfront has proven capable of pulling it off. For context, the company focused on entering the casual market in 2020 via the Storm8 and Candywriter acquisitions, but that doesn’t mean it is forgetting its older product categories, with the most recent Nanobit acquisition (our analysis here) being an example of further diversifying its Simulation, RPG, Action category. Clearly, Stillfront is looking to diversify both within its existing genres and expand into completely new genres, too.

Additionally, there are two more avenues of diversification. One of those is studio size, which often reflects the stage of maturity a studio is in. As Jörgen told us in our interview, Stillfront looks at three types of acquisitions: 1) big studios with $100m+ in revenue, 2) mid-sized studios with $20M to $100M in revenue, and 3) game assets.

The top tier is increasingly what moves the needle for the business and can also create meaningful, instant diversity into new genres and regions. The smaller categories present opportunities to onboard smart teams or new tech while they still have major upside, and it can be a way to dip a toe into the water for completely new types of games. Also, the size of deals also partially determines how the M&A financing gets done, with the smallest deals being mostly cash while the largest deals usually require more stock.

The second diversification avenue, and also the third type of acquisition, is one that Jörgen himself feels unsatisfied with: acquiring assets versus acquiring entire studios. As he explains it, “We have something where I'm not satisfied with what we've achieved so far. And that's asset acquisitions. It could be assets with a team, assets without a team, but I think that we can do so much more. We have seen so many opportunities with great products, high quality, well-ran products. Great gaming teams, but we basically don't share the view on the priorities for that particular studio, so then we have just left that, with one exception, because Kixeye actually was more of that, even though quite large scale.”

Strategy #3: Keeping studio operations decentralized, while still driving synergies throughout the group

Each of Stillfront’s 15 studios operates under a decentralized model, where they have their leadership, retain product ownership, and have more upside to capture from future payouts. Clearly, Stillfront wants to get out of their studios’ way and just let them do what they do best - make and live operate games. With decentralization, Stillfront allows these studios to operate independently, increase overall group operational efficiency, and broadly measure results against growth targets. Stillfront’s leadership is then enabled to fully focus on building and providing larger “platform” support across the group in addition to furthering future M&A efforts.

Decentralization works because the studios were already operating independently pre-acquisition, and Stillfront mostly respects studio autonomy. However, there is a common denominator that makes the decentralized model flourish under Stillfront: a homogenous business model across the entire company. Over Stillfront’s evolution, the team has focused on acquiring studios with F2P products that live operate with a game-as-a-service (GaaS) full stack. The GaaS model consists of four entities working closely together: a team that builds and operates the game, a tech stack supporting the game, a user acquisition team that scales the business, and finally a player support team that maintains player satisfaction. And this structure is maintained across every F2P team in the group, which is now the dominant business model across the group. This homogeneity results in some very impressive advantages.

Centers of excellence: Individual studios step up to spearhead developing the "best-in-class" features and procedures for a particular area in the mobile games business. Further, it builds genre mastery at a studio level, while elevating group personnel to be best-in-class too. This eventually results in sharing learnings and best practices across the whole group of studios, which is especially valuable in today’s mobile gaming market where specific genre innovation and evolution is increasingly inspired by looking at how other genres are succeeding. Eventually, this translates to benefiting the top line of the entire entity.

Seamless co-operation between studios: Similar to the point above, since all studios are operating games with the same underlying business model, terminology is identical, and best practices can be shared. Teams in a German studio can discuss and share learnings with a studio in Florida. In Jörgen’s words - “We work with different channels, Slack channels and other channels between different areas. We have something called StillBase, which is a knowledge base… every individual can go in and look for other people who are working with monetization in Bucharest for instance, or immediately finds that guy and can establish contact, getting into dialogue.” Pushing this even further would be cross-studio game development projects, and Stillfront seems to be pursuing that too. It was recently announced that Babil Games released the Arab version of Kixeye’s popular mobile game “War Commander: Rogue Assault”, and was published in collaboration with Kixeye and Goodgame Studios. That’s three studios using everything we’ve touched upon above to release highly localized versions of successful portfolio games to create more value to the group.

Distinct studio culture: Stillfront’s studios keep their own brand, culture, and identity when they join Stillfront. That said, all studios across the company learn to share a common set of values and principles that align daily work and decision-making. Each studio can work independently to create a strong culture that is not only true to its roots but also always hungry to achieve better results. It also creates healthy competition between studios, where cross-studio learnings are reinvested to creating the best culture, retaining the best talent, and building the best games.

Buying time for building new titles: With all the benefits attached to centers of excellence, seamless cooperation between studios, and distinct studio cultures, the decentralized model allows for new ideas to flourish within studios without the intervention of HQ. That said, new ideas need time to fully evolve into great games - and time is really of the essence in a creative industry like ours. While Stillfront’s financial flexibility plays a key role in buying this required time, it is a key responsibility that HQ needs to ensure of in the decentralized set up. After all, there is no game in any acquired unit that can be live operated forever.

All that being said, there are a couple of risks involved with a decentralized model. The largest risk is financial. Growth is mostly reliant on striking new, bigger, and better deals. Therefore, overpaying for a major deal that fails to deliver, due to poor live operations, new releases flopping, or cultures clashing, can negatively impact the entire growth engine. While Stillfront’s Stillbase seems like it helps de-risk this aspect, being highly selective, accurate, and disciplined is required throughout the M&A process. And all this is underscored by the fact that the acquired units will have to function independently once they’re under Stillfront’s umbrella.

Second is a risk related to leadership talent. If the acquired studio founders decide to leave and the bench of leadership talent isn’t deep, the decentralized model can struggle. To incentivize founders, acquirer's equity in Stillfront matters. Since Stillfront is now publicly traded, its stock has immediate liquidity, and parties on both sides of the acquisition table know that their collective work is helping create something even bigger. This is also reflected in the way Stillfront usually structures its deals - a majority stake is paid out on a cash/equity basis, while the remaining minority stake is earned through equity in Stillfront only when certain EBIT goals are met by the acquired unit. What if the founders still leave? More often than not, their heart wasn't in it anyway, and it's probably better to train people within the studios to become its future leaders.

The third risk is culture related. Bringing studios from different countries and cultures together requires ongoing facilitation so that studios can better balance retaining their own culture while staying aligned with Stillfront’s higher-level objectives. The possible negative effects of decentralization on culture are fairly obvious, but Jörgen’s thoughts confirm that maintaining a healthy balance between overall group culture while preserving individual studio culture is a top of mind issue at Stillfront and it will be an ever-evolving effort. Jörgen’s thoughts on culture - “There are differences between the studio's cultures on a more fine granular level, and that's all good. If you tried to have a conformed culture in a studio in Jordan, Amman, the same as in San Francisco, in Victoria, Canada, in the north of Sweden, in Bucharest, Sofia, and so on, I would doubt that works very well because we are different as people; we are brought up in different cultures; there are differences that need to be there. But if we can identify some common things, being open, and being humble is very important.”

All in all, each of these risks will continue to persist, but they might even morph into different shapes and forms given how Stillfront continues to evolve. The more important thing is that Stillfront is aware of these potential issues and actively working to mitigate them. We can confidently say that the way Stillfront is executing its decentralized model is working very well for now, and if past performance is any indicator of future results then it will continue to excel on this front.

Looking Ahead for Stillfront

Stillfront’s future consists of relatively clear knowns and unknowns. What’s known is the company’s ambition, long-term mindset, growth strategy, decentralized proclivity, and approach to culture and knowledge sharing. In essence, we know the general framework for how and why decisions get made. That means that Stillfront’s future can likely be boiled down to “more of the same, but bigger, faster, better, and more diversified.”

Of course, everything else is an unknown. Understanding the company’s strategy — especially in a mostly growth-by-acquisition business — tells us nothing about what will be acquired next, when, or at what terms. The same goes for specific game launches. The details are entirely up in the air, and not even Stillfront’s leadership can know exactly what the business will morph into. Is that a bad thing? Not at all, as long as opportunities abound and management remains diligent. Of course, there’s a difference between strategy and competitive advantage, which we didn’t touch on much. That’s because Stillfront doesn’t yet hold many traditional competitive advantages (like major network effects, powerful brands, flywheels, or being a low-cost producer), at least in big ways — although perhaps at greater scale this can change — but it holds many micro-advantages that result from its the wide variety of things it owns.

To get a bit more specific, these are some tactics we think Stillfront will likely pursue:

- Organic growth will remain important (if not grow in importance), but growth by acquisition will remain the company’s primary means of scale.

- Stillfront will continue to pursue genre, geographic, and size diversity. Profitability and stable leadership will also stay important.

- The company will continue to use a relatively conservative mix of cash, debt, and stock to acquire others, but the exact levers used will change depending on the specific deal and the current state of the business, share price, interest rates, etc.

- Acquisitions will likely get more frequent, like we’re seeing in 2020. Even though the business will continue to strike smaller deals, larger ($100+ million) deals will grow in frequency and ultimately become what moves the needle most. We think that there’s plenty of ways to add greater diversity, but it will get tougher to find and win needle-moving deals at great prices.

- Even though the business will stay mostly decentralized, Stillfront will improve its efforts to share learnings and best practices across the business.

- It’s also possible that Stillfront divests certain studios one day, but we don’t think that’s likely anytime soon.

Will Stillfront succeed in its quest for further scale? We think so. Winners tend to keep on winning, and Stillfront’s strategy definitely can work over multiple years. The industry is massive, and Stillfront remains a relatively small business.

There are risks, though. One risk is creative. If the company’s studios stop creating great games, then the business unravels. Given the company’s track record and increased diversity, however, we think existential creative risks are minimal unless broader disruption occurs. Of course, there is an opportunity to ramp up internal game production, which at minimum is another way to diversify, but it’s also a source of potential growth that many are overlooking. There’s a very real risk that these efforts don’t pan out, which limits organic growth, but as Stillfront acquires more studios the odds of a new breakout hit likely increases. Time will tell.

The other risk, which we mentioned earlier, is financial. A bet on Stillfront, so to speak, is just as much a bet on the pilot as it is the plane. Stillfront’s outsized success so far is a result of Jörgen and team’s smart capital allocation, and any future outsized success or failure will also be a result of smart capital allocation. We think management is diligent, but as moving the needle increasingly necessitates larger deals, it means the potential upside and downside of each deal grows. If Stillfront overpays for a large business that dramatically underperforms, it will send ripple effects down the entire business — slowing growth, providing less cash flow, making shares less valuable (which reduces the appeal of acquiring with equity), and potentially adding unnecessary debt or dilution. So far so good, and there’s little reason to think Stillfront will make a huge mistake, but it’s important to remember that the growth engine holds potential fragilities. Many seemingly great growth-by-acquisition companies have flamed out because of big bad deals. It’s also going to be extremely hard for management to unlock value at anything close to the trajectory we’ve seen over the past couple years — especially as stock multiples rose following accelerating growth — so it’s important to keep expectations in check.

All in all, if Stillfront effectively executes and continues winning attractive deals, there’s little reason why it can’t become a much larger gaming business, especially in mobile. The company already has made tremendous progress, but it remains half the size of Zynga and a tenth the size of EA. If management continues making savvy decisions, then the gap can continue to close. However, the gap won’t close because out outsized IP but rather a system that breeds diversity, consistency, and diligence in a way others can’t easily match. That’s the special Stillfront way.

Conclusion

Stillfront is best understood through the lens of its history and strategy, a game plan that continues to play out in bigger, higher stakes ways. We think the company’s focus on scaling high margin, recurring revenues through long lifecycle games is wise, and we admire the team’s savvy and diligence when it comes to growth-by-acquisitions. It’s certainly worked exceptionally well so far! Similar to Stillfront’s past, the company’s future is dependent on how well leadership executes on that strategy, because without it the edge that makes Stillfront special and so valuable begins to fade away. That said, even if the pace or attractiveness of deals ebbs and flows, we currently see no reason why Stillfront can’t continue striking notable deals for many more years. There’s only so many large acquisition targets, to be fair, but there’s plenty of growth left from here as long as the industry holds steady and management doesn’t screw up a major deal.

Importantly, Stillfront is more than just an acquirer; its approach to company building isn’t common in the industry, and its approach to sharing knowledge and incentivizing independent teams should be studied more widely. At minimum, digging into Stillfront is a reminder that not all games companies need to chase the next mega-hit; diverse, consistent, and profitable approaches — even if at smaller scales on a per game basis — can still turn into something big and praiseworthy. And, of course, if management continues to defy expectations and scale this consistent profit generator to new heights, Stillfront truly could become much larger than observers expect. In other words, despite remarkable performance over the past few quarters and years, maybe Stillfront still is the underrated dark horse that many now recognize it was.